GBP/USD Prices, Charts, and Analysis

- Gilt yields push sharply higher on renewed UK rate hike expectations.

- IMF does a 180 on UK growth prospects.

- Little in the way of UK data next week.

Recommended by Nick Cawley

How to Trade GBP/USD

UK headline inflation fell back into single digits, figures showed this week but failed to meet analyst expectations, while the core reading rose to levels last seen over three decades ago. While elevated energy prices started to fall out of the reading, food prices, in particular, continued to rise, putting the squeeze on consumers. The financial markets are forecasting that the Bank Rate will rise from its current level of 4.5% to at least 5% over the next couple of meetings with some hawkish forecasters suggesting that the UK central bank will have to go to 5.5% to dampen down sticky price pressures.

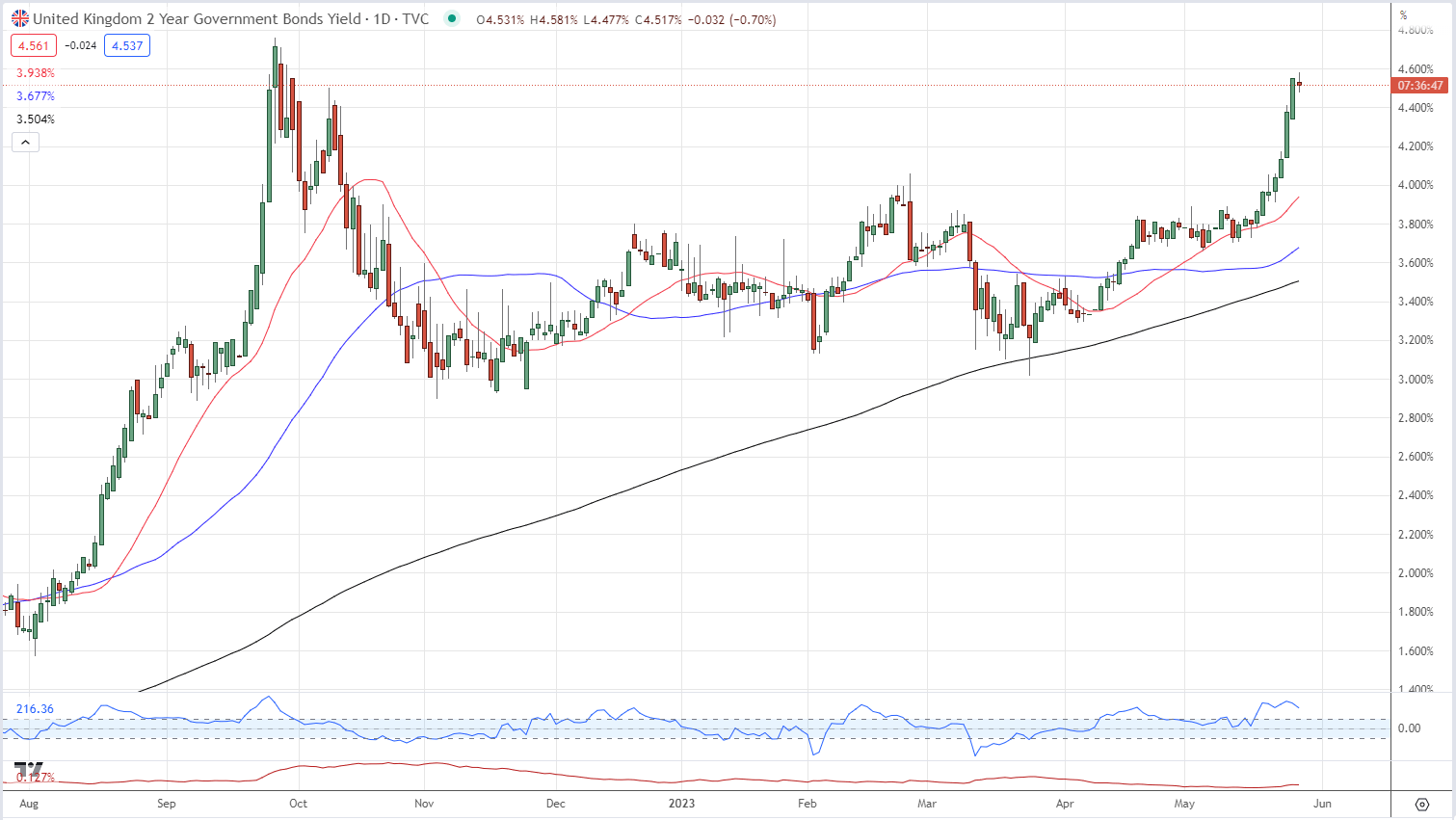

The UK gilt market took its cue from the inflation report and the subsequent elevated rate hike expectations. Yields across the curve rose to multi-month highs as market participants demanded more risk premiums for their money. The UK 2-10 gilt curve inverted further, a warning that the UK is likely heading towards a recession, in contrast to the IMF’s latest update. The International Monetary Fund (IMF) this week upgraded the UK’s growth prospects and said that a recession was now unlikely. Staff forecasts now see the UK economy expanding by 0.4% in Q2 compared to a contraction of 0.6% predicted by the Fund back in January. The latest S&P UK PMIs also predict that the UK economy will expand by 0.4% in Q2.

British Pound (GBP/USD) Latest: IMF U-Turn, UK PMIs, US Debt Talks

UK 2-Year Gilt Yield Daily Chart

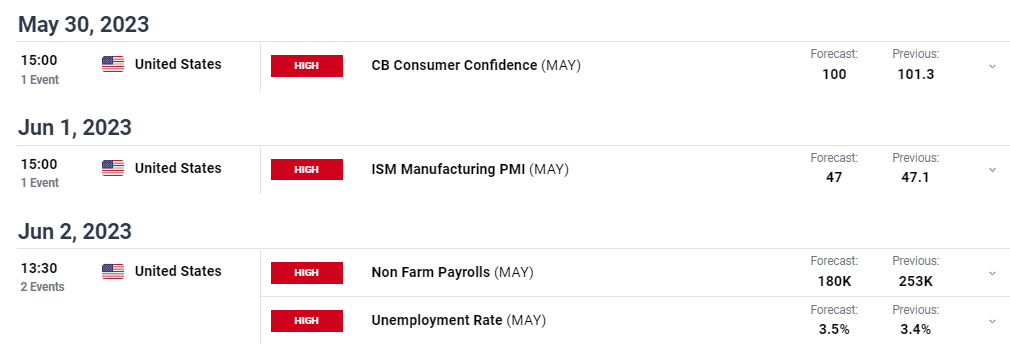

Next week’s economic calendar shows little in the way of any meaningful UK data or events. The US docket however shows a handful of high important releases with next Friday’s US Jobs Report the pick of the bunch. The US labor market remains robust and is one of the reasons why inflation in the US is refusing to make any meaningful move lower.

For all market-moving events and data releases see the real-time DailyFX Calendar

To round off next week’s events, the US debt ceiling negotiations enter what is likely to be the home stretch as the X-date, June 1 nears. The latest chatter from the US is that the two sides are now much closer to reaching an agreement, although it remains to be seen if they can get any deal over the line in time.

Debt Ceiling Blues, Part 79. What Happens if the US Defaults?

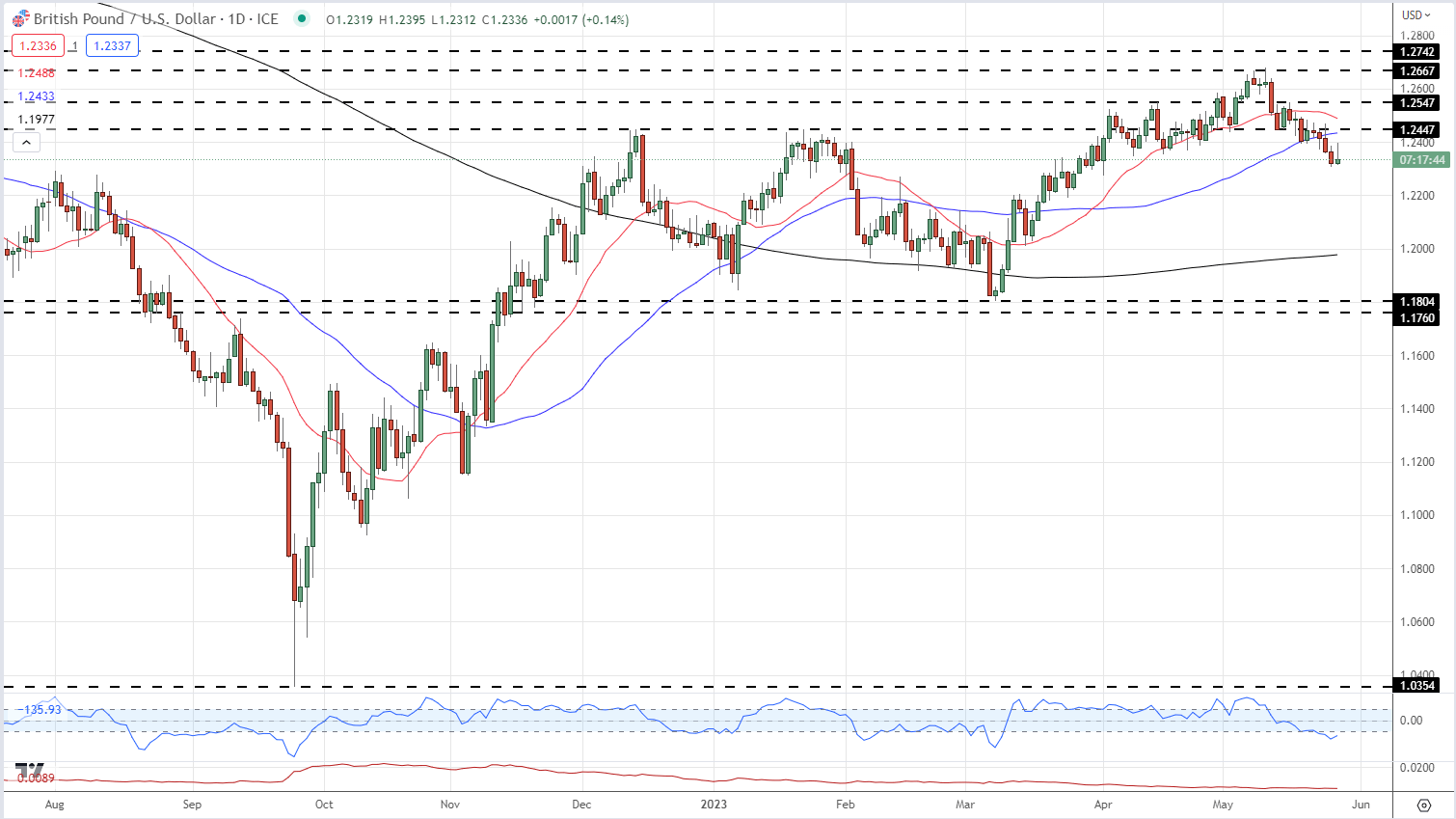

Cable (GBP/USD) will remain under the influence of a strong US dollar and heightened UK rate expectations next week. The four-day week will likely see increased GBP/USD volatility around US data releases and debt ceiling talks. The pair tested and rejected the 1.2300 handle yesterday and today and while this big figure remains in view it is reasonable to expect that it will be tested again. Adding to the negative outlook, GBP/USD now trades below both the 20- and 50-day moving averages, although the pair look oversold using the CCI indicator. Volatility in cable remains low and this looks set to change with all the data releases and macro events out next week.

GBP/USD Daily Price Chart – May 26, 2023

Chart via TradingView

| Change in | Longs | Shorts | OI |

| Daily | -7% | -4% | -6% |

| Weekly | 10% | -18% | -3% |

Retail Trader Signals are Mixed

Retail trader data show 57.83% of traders are net-long with the ratio of traders long to short at 1.37 to 1.The number of traders net-long is 2.04% lower than yesterday and 1.43% lower from last week, while the number of traders net-short is 1.79% lower than yesterday and 7.38% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests GBP/USD prices may continue to fall. Positioning is less net-long than yesterday but more net-long from last week. The combination of current sentiment and recent changes gives us a further mixed GBP/USD trading bias.

What is your view on the GBP/USD – bullish or bearish?? You can let us know via the form at the end of this piece or you can contact the author via Twitter @nickcawley1.

Comments are closed.