S&P 500 FORECAST:

- S&P 500 moves without strong conviction as traders avoid making large directional bets on the index ahead of Friday’s U.S. employment survey

- February nonfarm payrolls are forecast to clock in at 205,000, following January's 517,000 increase

- A hotter-than-expected report is likely to be bearish for stocks to the extent that it would push Fed interest rate expectations higher

Recommended by Diego Colman

Get Your Free Equities Forecast

Most Read: S&P 500 and Nasdaq Outlook: Is Powell’s Testimony a Game Changer?

The February U.S. jobs report will be heavily scrutinized on Friday for clues about the momentum of the economy and to determine whether January's extraordinary payroll gains were a blip or a trend. That said, we may be at a point when good news is bad news, and when bad news is good news for stocks and other risk assets.

Last month, U.S. employers added 517,000 workers, more than twice as many as projected and the most since July 2022, bringing the unemployment rate to 3.4%, the lowest level in 53 years. Under normal conditions, a solid labor market would be a welcome development, but right now excessive strength is counterproductive insofar as it is exacerbating inflationary pressures by boosting wages and sustaining strong consumption.

For tomorrow’s nonfarm payrolls survey, the American economy is forecast to have created 205,000 jobs, but the ADP and ISM services reports suggest we could be in for an upside surprise.

NONFARM PAYROLLS REPORT EXPECTATIONS

Source: DailyFX Economic Calendar

In his semi-annual appearance before Congress this week, Fed Chairman Jerome Powell said that the central bank’s terminal rate is likely to settle higher than initially anticipated and that the institution is prepared to accelerate the pace of hikes if the totality of incoming information indicates faster tightening is warranted. A sturdy NFP print will undoubtedly meet that criterion, sealing the deal for a half-point hike at the March FOMC meeting.

For monetary policy jitters to abate and stocks to stage a meaningful rebound, softer macro figures are required soon; that’s the only way for the Fed to start embracing a less aggressive stance and for investors to prepare for an eventual pivot. If the data does not cooperate and the economy maintains the impetus seen earlier in the year, interest rate expectations will continue to rise, undermining risk assets across the board.

Focusing on the S&P 500, the index managed to recapture the 4,000 level in the morning trade but is moving without strong conviction on Thursday, as traders avoid taking large directional positions ahead of Friday's NFP survey at 8:30 am NY time.

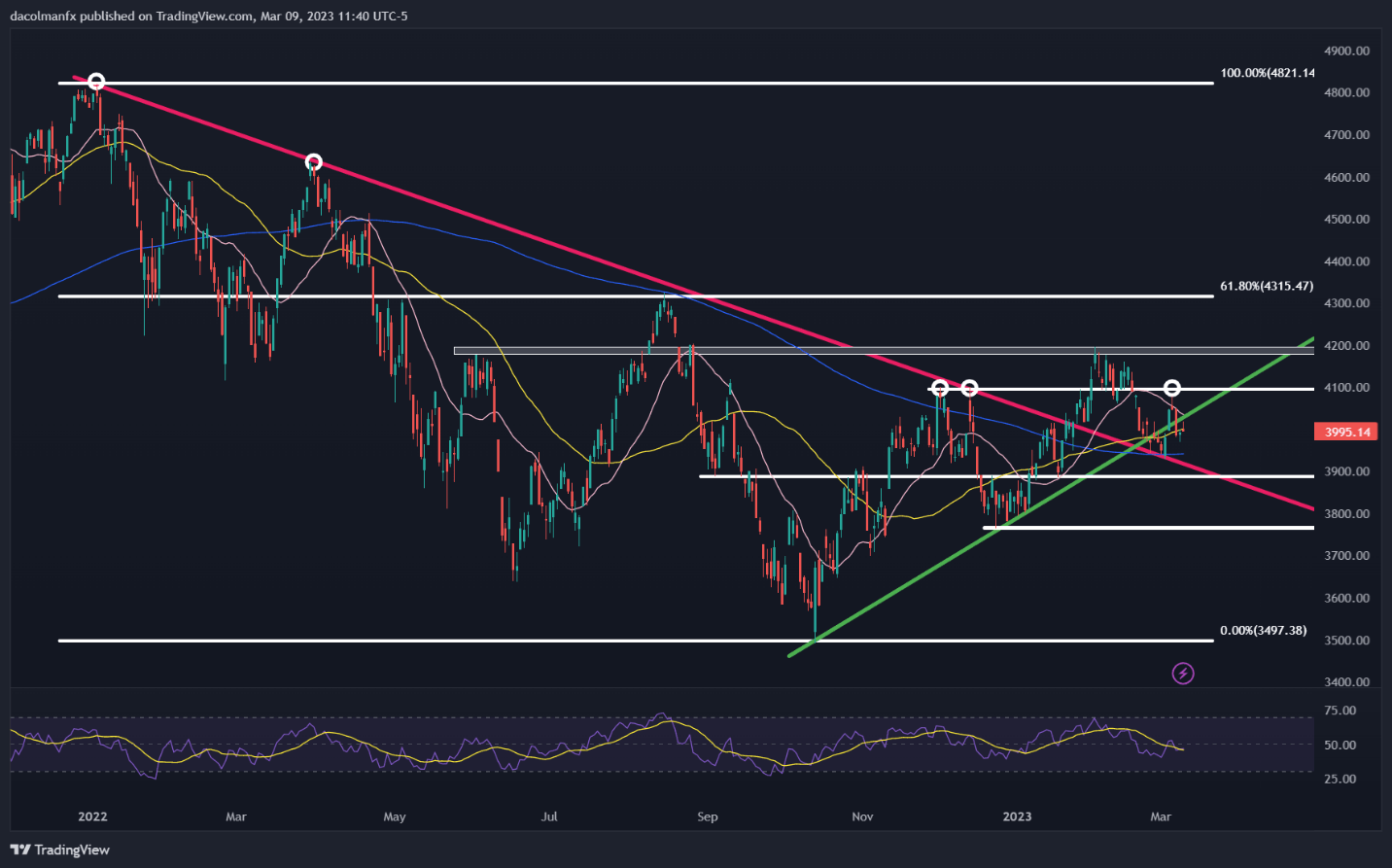

Looking at the daily chart, prices remain below an important trendline that has guided the recovery off the October 2022 lows. This is an important resistance that currently sits around 4,025. If buyers regain control of the market and push the index above that barrier, we could see a rally towards 4,100, followed by 4,200. On the flip side, if the S&P 500 turns lower, initial support is found around the 200-day simple moving average and 3,890 thereafter.

| Change in | Longs | Shorts | OI |

| Daily | 1% | 2% | 1% |

| Weekly | -12% | 3% | -5% |

S&P 500 TECHNICAL CHART

S&P 500 Chart Prepared Using TradingView

Comments are closed.