OIL PRICE, CHARTS AND ANALYSIS:

Recommended by Zain Vawda

Get Your Free Oil Forecast

Most Read: What is OPEC and What is Their Role in Global Markets?

Oil prices continued their renaissance this week finally breaking out of a two-month range. Initially I had concerns that the breakout may be short lived following lackluster Chinese data, however improving sentiment and a softer US CPI print have helped Oil post a 2.5% gain in the last two days.

The US Dollar has faced significant selling pressure this week further compounded by yesterday’s softer CPI print. Market participants seem resigned to the fact that a July rate hike remains on the cards but seem to be growing more confident that the July hike could spell the end of the US Federal Reserve's hiking cycle. The Dollar Index (DXY) is at risk of surrendering the psychological 100.00 mark as it trades at lows last seen in February 2022, is this the start of a larger downward move for the USD?

CHINESE DATA, IEA MARKET REPORT AND THE IMF

Chia remains interesting as despite a stuttering recovery Oil data released last month revealed that demand for oil remains strong. This morning brought Chinese import and export data for the month of June which both came in well below estimates. The data and particularly the export number could be viewed as a sign of a slowdown in the global economy while at the same time giving the Chinese government further food for thought moving forward.

We have already heard mounting speculation that China’s top leaders may announce a massive stimulus package at a key meeting later this month. This could provide a welcome boost not just for China but Global economies as well.

For all market-moving economic releases and events, see the DailyFX Calendar

The IEA released the oil market report for July this morning with the IEA seeing global oil demand rise by 2.2 million bpd in 2023 and reach a record 102.1 million bpd. However, the headline may be slightly misleading as persistent macroeconomic headwinds, a deepening manufacturing slump, have led the IEA to revise their 2023 growth estimate lower for the first time this year, by 220 kb/d. This does seem more realistic given the recent decline in global PMI data which suggests a global slowdown is on the cards for the second half of 2023.

As mentioned above Chinas oil demand has remained robust despite the stuttering recovery and the IEA attributed this to surging petrochemical use which is expected to see China account for 70% of global gains.

The International Monetary Fund (IMF) also released some comments this morning expressing their surprise at the largely positive global growth numbers from Q1. The IMF also expressed their belief that a ‘softer landing’ remains a possibility as inflation begins to decline but cautioned G20 countries of the risks to the financial sector as a result of the hiking cycles globally. The IMF did point to a slowdown in momentum including Chinas recovery which could prove a threat for oil demand in the second half of the year.

Discover what kind of forex trader you are

ECONOMIC CALENDAR AND EVENT RISK

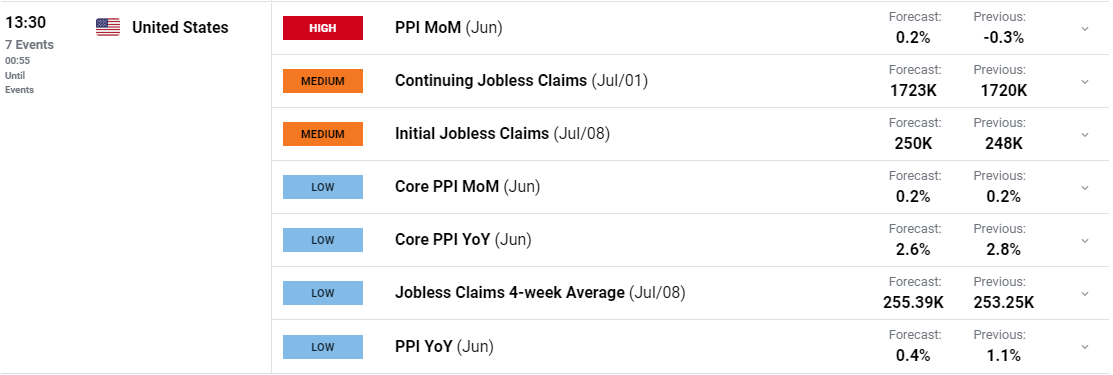

Later today we have more high impact data out of the US with PPI likely to be more important following a soft CPI print yesterday. A softer PPI print could indicate that a continued decline in price pressures and bode well for inflation numbers moving forward. This could add to the Dollar's weakness and likely give Oil prices further impetus to push higher.

Alternatively, a higher-than-expected PPI print could see some buying interest in the US dollar return and thus pushing Oil prices lower. Either way it promises to be another interesting US session.

For all market-moving economic releases and events, see the DailyFX Calendar

TECHNICAL OUTLOOK AND FINAL THOUGHTS

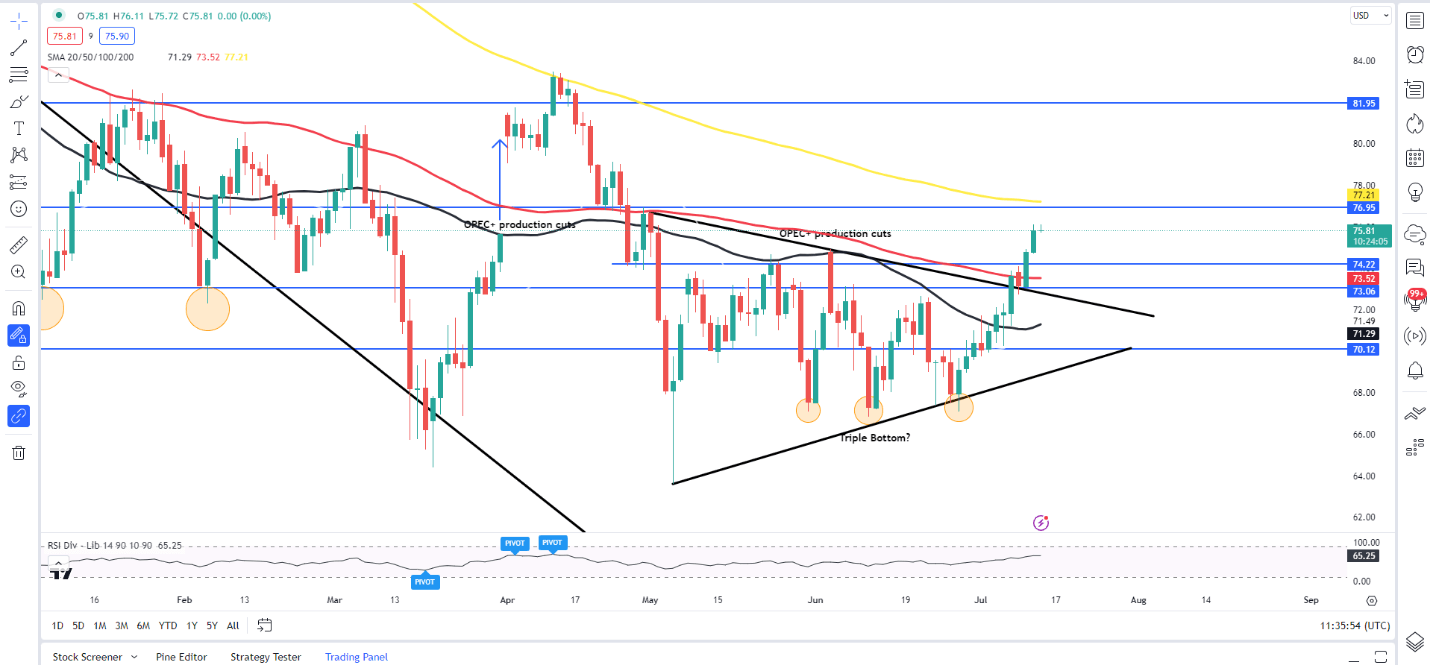

From a technical perspective both WTI and Brent appear to be running out of steam with the RSI approaching overbought territory. The recent rally and breakout of the symmetrical triangle pattern leaves WTI just of the 200-day MA with a catalyst likely needed for the rally to continue from current levels. The US PPI data could provide a catalyst of sorts pushing WTI toward the 200-day MA around $77.20 before a potential retracement.

WTI Crude Oil Daily Chart – July 13, 2023

Source: TradingView

A breakdown form here however could see Oil find support at the break of the triangle which coincides with the 100-day MA around the $73.50 mark.

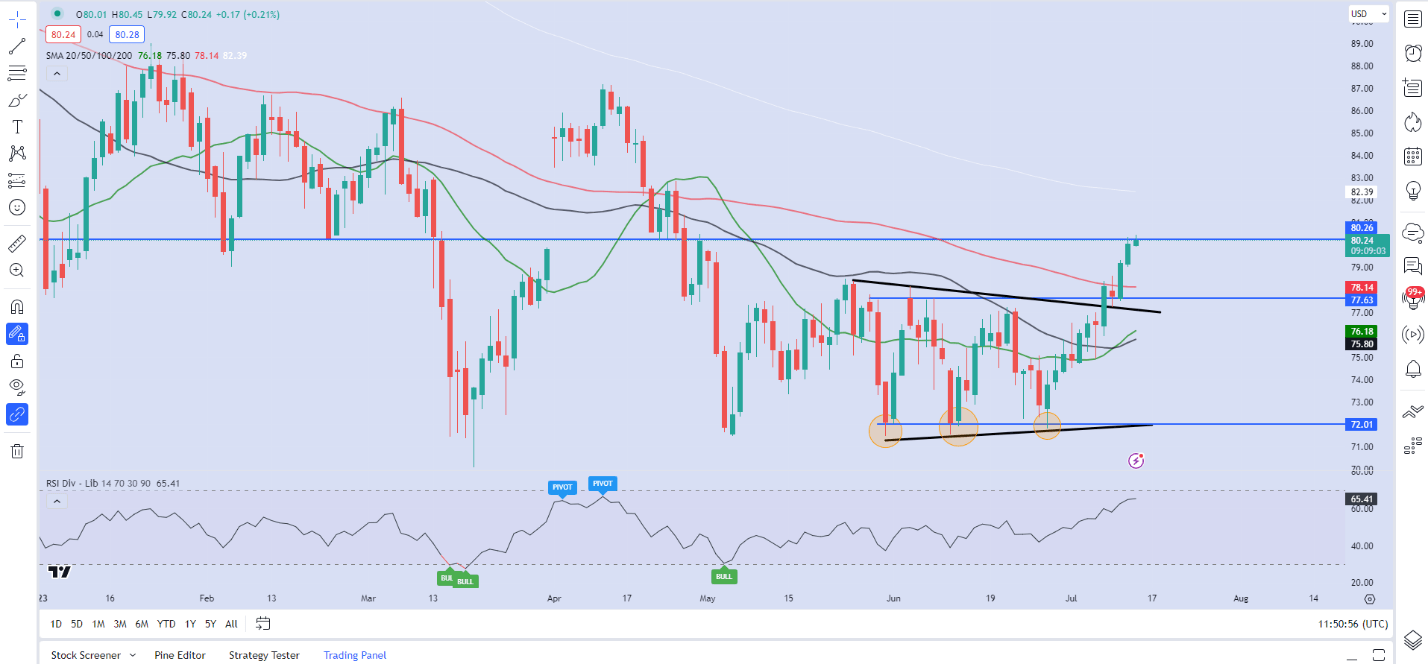

Brent Oil Daily Chart – July 13, 2023

Source: TradingView

Taking a quick look at Brent Crude and we can see a similar pattern in play following a break of the triangle pattern. Brent is currently trading around the psychological $80 a barrel mark. The last time brent traded above the $80 a barrel mark was April 2023. Should today’s daily candle fail to close above the $80 mark we could be in for a retracement toward the 100-day MA resting around the $78.10 mark before the upside rally continues.

It is important to note that macro developments are likely to play a huge role in the next move for Oil prices as we head deeper into Q3.

Recommended by Zain Vawda

Get Your Free Top Trading Opportunities Forecast

Written by: Zain Vawda, Market Writer for DailyFX.com

Contact and follow Zain on Twitter: @zvawda

Comments are closed.