US Dollar, USD/JPY, Japanese Yen, NZD/USD, RBNZ, AUD/USD – Talking Points

- The US Dollar wilted across the board today as markets contemplate US CPI ahead

- The Japanese Yen strengthened more than most as the BoJ moves into view

- The RBNZ pause its hiking cycle today. If CPI is soft, will the Fed do the same?

Recommended by Daniel McCarthy

Get Your Free USD Forecast

The US Dollar struggled to find traction going into the Wednesday session despite Treasury yields stabilising after sliding in the prior sessions. The largest losses were seen against the Japanese Yen and the Australian Dollar.

After eclipsing 145 last week, USD/JPY has crashed below 140 today as the timeline of a possible tilt from the Bank of Japan is being re-assessed by the market. They will meet to decide on monetary policy on July 28th.

At the same time, there is a degree of nervousness ahead of crucial US CPI data, potentially undermining USD.

A Bloomberg survey of economists is anticipating that the year-on-year headline inflation gauge will continue to ease and print at 3.1% later today. Well below the 4% prior reading.

The benchmark 10-year Treasury note is yielding close to 3.95% after almost touching 4.10% at the start of the week.

US CPI will be a critical piece of the monetary policy for the Fed at its Federal Open Market Committee (FOMC) meeting on July 26th.

In the Asian session, the Reserve Bank of New Zealand (RBNZ) left its overnight cash rate (OCR) unchanged at 5.50% at their monetary policy committee (MPC) today.

NZD/USD initially dipped but recovered soon after as the interest rate market moved toward a less restrictive policy further out on the curve to potentially improve the domestic economic outlook.

AUD/USD was also supported by comments from Reserve Bank of Australia (RBA) Governor Philip Lowe that were viewed as less hawkish than the language in last week’s statement on monetary policy.

Crude oil has made a 2-month high with the WTI futures contract trading as high as US$ 75.14 bbl while the Brent contract touched US$ 79.75 bbl. Gold also gained on the weaker US Dollar, overcoming US$ 1,940 today

APAC equities had a mixed day with all the main Japanese indices sinking with a stronger Yen while Hong Kong’s Hang Seng Index (HSI) saw some decent gains.

Yesterday’s pro-growth commentary from President Xi Jinping might have assisted the outlook for the world’s second-largest economy.

While US CPI is likely to be the main focus for the market today, Bank of England (BoE) Governor Andrew Bailey will also be speaking and may provide some volatility.

The full economic calendar can be viewed here.

Recommended by Daniel McCarthy

How to Trade USD/JPY

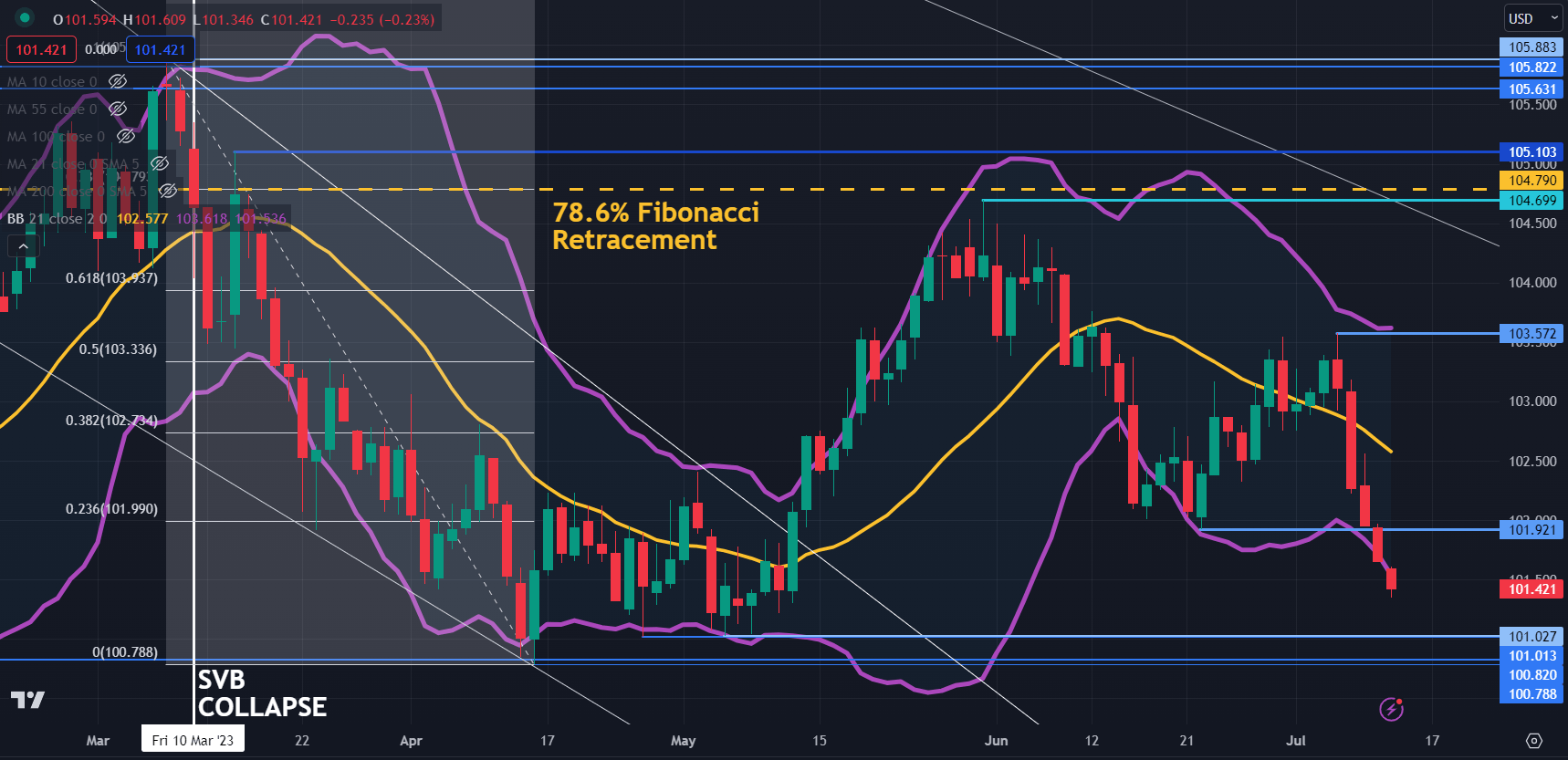

DXY (USD) INDEX TECHNICAL ANALYSIS

The DXY (USD) index made a 2-month low today and it might test potential support in the 100.80 – 101.00 area where there are a series of prior lows.

The recent sell-off broke below the lower band of the 21-day simple moving average (SMA) based Bollinger Band. A close back inside the band might signal a pause in the bearish run or a potential reversal.

On the topside, resistance could be offered at the breakpoint of 101.92, ahead of the recent peak of 103.57.

Chart created in TradingView

— Written by Daniel McCarthy, Strategist for DailyFX.com

Please contact Daniel via @DanMcCarthyFX on Twitter

Comments are closed.