S&P 500, VIX, Dollar, Fed Funds Rates and Event Risk Talking Points:

- The Market Perspective: EURUSD Bearish Below 108, Dow Range Between 34,200 and 33,200

- The S&P 500 and Dow produced ‘inside days’ this past session, working their way more deeply into congestion patterns that may prove difficult to break

- With only a few high profile events this week (eg UofM sentiment) and next (eg US CPI), volatility will struggle to form trend…unless there is an elemental development in ‘risk trends’

Recommended by John Kicklighter

Get Your Free Top Trading Opportunities Forecast

It’s possible for markets to develop trends through the organic development of a bullish or bearish fever, but motivation through a distinct fundamental event or theme tends to be more reliable and easier to track. Unfortunately for those that look for hearty swings in the market – much less those that seek out trends – there is a critical lack of high-profile event risk through the end of this week and even into next week. With a significant cooling in the market’s attentiveness to small developments in themes like monetary policy speculation, recession fears and external matters (trade wars, actual wars, etc), there will be a greater propensity towards developing congestion or to experience short-lived bouts of volatility that struggle to facilitate traction into earnest trend. That is not to say it is impossible to generate a bigger move, but the market conditions seem to be skewed in that direction.

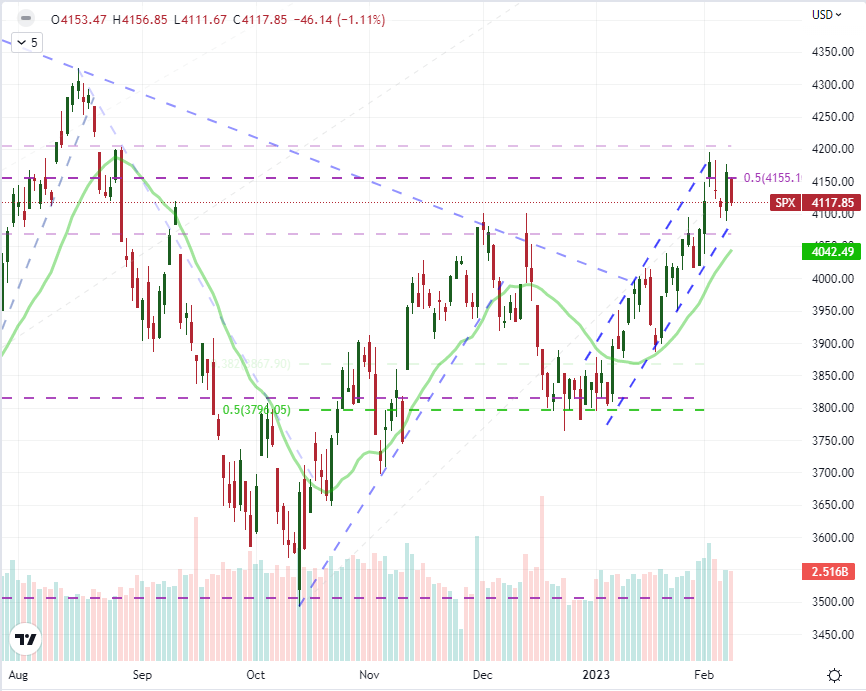

Evolution of market conditions from range to breakout to trend are normal, and an industrious trader would adapt to the given conditions. For practical application, the S&P 500 reflects the shifting perspective according to time frame well. On a monthly chart, the larger bull trend of the past 15 years is generally in place. On the daily chart, the 2022 bear market is dealing with the higher lows from October to establish a prevailing direction. Lowering the time frame to a four-hour chart, we have the rising trend channel of the past six weeks but also the wedge that has developed just over the past week…right at the midpoint of the 2022 range. The Dow’s resistance to a broader trend is even more distinct with two months of broader congestion – a wedge that now presents barriers at 34,300 and 32,300. Technical barriers are not sacrosanct; but if there is an attempt to breach a key level without a very prominent catalyst, holding a very high degree of skepticism would be warranted.

Chart of S&P 500 with 20-Day SMA and Volume (Daily)

Chart Created on Tradingview Platform

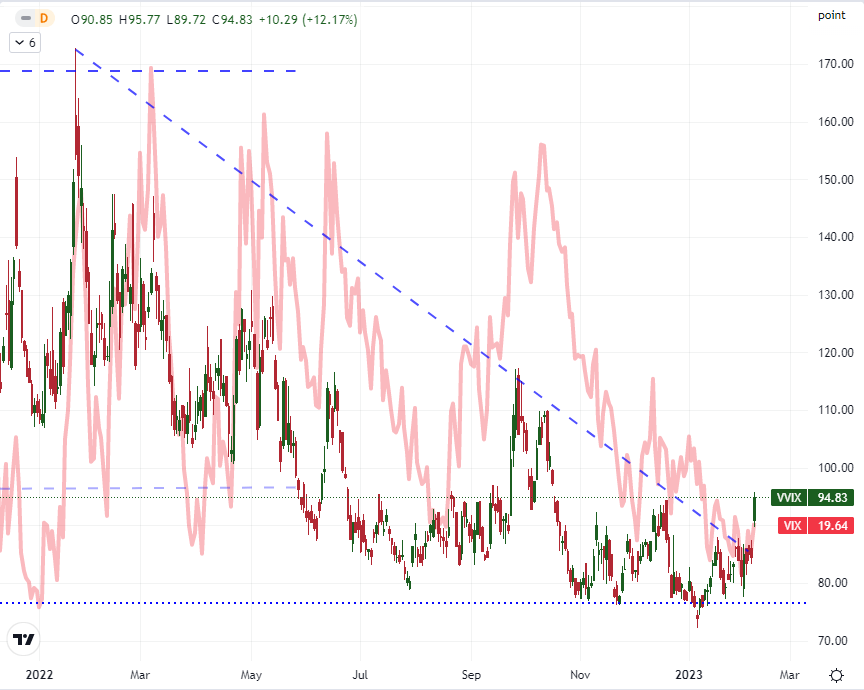

Historically, the 6th week of the year – which we are currently traversing – has averaged a distinct jump in the level of implied (expected) volatility via the VIX index. While the activity gauge has held closer to the 20 level and not indulged the drop to 12 month lows plumbed last week, the measure is still noticeably deflated. That said, for the equities (S&P 500 specifically) based measure, there has been a notable development in the ‘second derivative’ measure that is the VVIX. The so-called ‘volatility of volatility’ measure charged to a near four month high Wednesday which is out of the blue but worthy of monitoring as it suggests there is a higher risk of a sudden change in activity levels. Meanwhile, volatility measures across a range of alternative markets (yields, commodities, currencies, emerging markets, etc) has experienced similar moderation. These readings have a fairly poor track record as leading indicators, but they are reasonably well-tuned for reflecting current conditions.

Chart of VVIX Volatility of Volatility Index Overlaid with VIX Volatility Index (Daily)

Chart Created on Tradingview Platform

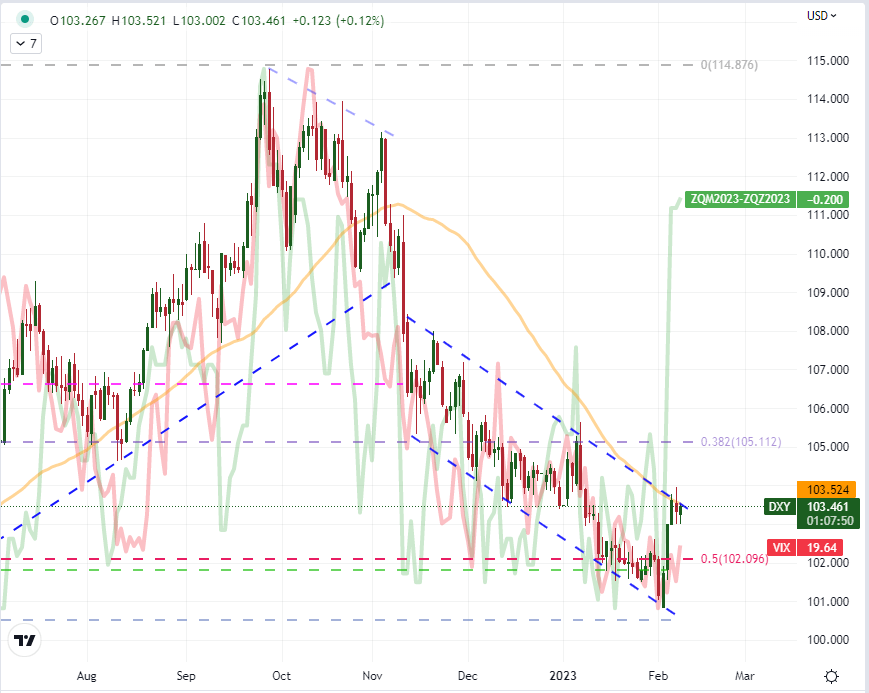

Meanwhile, applying the throttling effect to the US Dollar may amplify the weight of proximate technical levels for aggregate measures along with key majors. The rally the Greenback (DXY Index) has earned this past week helped stave off a renewed leg of a larger bear trend that was tentatively slipping below the midpoint of the 2021-2022 range (102.10 for the DXY). However, that rebound has found capable resistance in the combination of the 50-day SMA and the resistance of a three-month descending trend channel. The justification of this upswing drew heavily upon the upswing in the market’s forecast for the Fed’s terminal rate. Having reached a 5.1 percent implied forecast for June to match the FOMC’s own forecast, there isn’t much further discount for the market to work off. It’s possible that the rate hike still priced through the second half of 2023 can offer the Dollar a further ‘relief rally’, but that is a small window. The more potent spark would be a sudden flare up in volatility, which is a more common event historically. Otherwise, we will likely be waiting until next week’s consumer price index (CPI) release for a definitive update on the rate speculation theme.

Chart of DXY Dollar Index with 50-Day SMA, Overlaid with VIX and Market Implied Fed Cuts (Daily)

Chart Created on Tradingview Platform

For scheduled event risk through the final 48 hours of trade this week, the docket is particularly light. Thursday’s session has a few highlights that could generate localized volatility or perhaps carry the opportunity of grey swan blowback. Germany inflation is a leading figure for ECB rate speculation and the Mexican central bank can surprise at its monetary policy event, but the scheduled earnings report from Adani could be an unexpected spark given the dramatic fall in value for the Indian behemoth following accusations of financial malfeasance. For more reliable event risk, the Chinese inflation statistics, UK economic activity (official 4Q and forecast from NIESR) and the US consumer sentiment survey from the UofM are on tap Friday. I won’t hold my expectations for systemic trends through global capital markets through any of this data, but it can certainly generate serious localized volatility.

Top Global Macro Economic Event Risk for the Next 48 Hours

Calendar Created by John Kicklighter

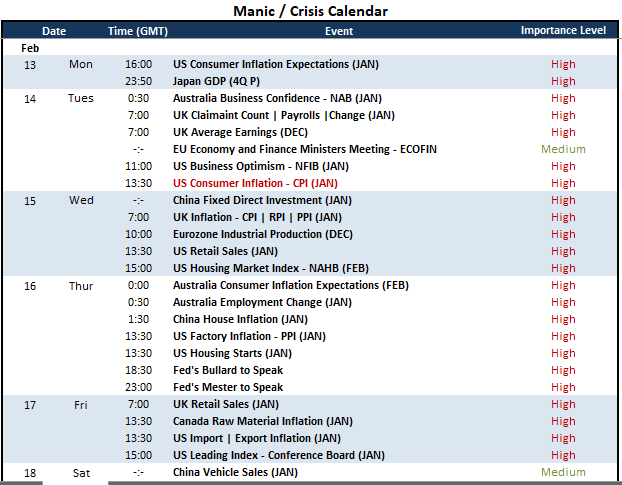

Looking a little further ahead, next week’s docket has a higher density of higher profile event risk; but it is far from the depth of what we were wading through last week. Top listing through the entire week has to be the US CPI release for January. While not the Fed’s preferred inflation reading, it is the market’s and that is where volatility is liberated. After a series of months whereby the inflation reading has experienced substantial deceleration, the expectation will naturally be another step down. That makes the greater impact for a surprise from an uptick or ‘higher than expected’ reading. Then again, with the Dollar enjoying a bounce recently owing to its alignment between market and Fed forecasted terminal rate, a softer reading could restore the common market discount and weigh the Greenback – and possibly even recharge equities. Outside of that reading, Fed speak, US retail sales, US housing market activity, UK inflation and Australian employment data is on the docket for volatility potential.

Top Global Macro Economic Event Risk for Next Week

Calendar Created by John Kicklighter

Discover what kind of forex trader you are

Comments are closed.