Short DAX as German Fundamentals Turn Sour

The DAX has rise around 38% from the October 2022 low, fully retracing the 2022 major sell-off as European equities became relatively more attractive than US equities with their lower price-to-earnings ratios. The ECB was late to join the rate hiking cycle and naturally took a more gradual approach when it came to tightening overall financial conditions.

Recommended by Richard Snow

Staying with Europe, see what Q3 may have in store for EUR

Data Revisions Plunge Germany into a Technical Recession in Q1 2023

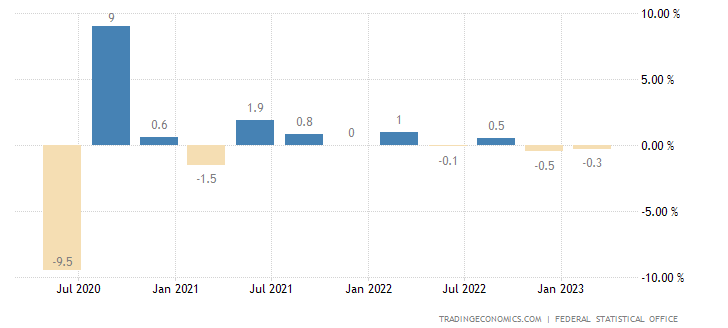

The broader EU economy had been spluttering along until revised Q1 data and Q4 2022 data suddenly placed not only Germany but also the Euro Zone into a technical recession. A technical recession is defined as two consecutive quarters of negative GDP growth. However, it was even worse economic data out of Germany that led to the overall downward revisions. The industrial powerhouse followed up a Q4 contraction of 0.5% with a further contraction of 0.3%.

German GDP Growth

Source: tradingeconomics

German exports have suffered during this period of slowing global growth – a deliberate result of tighter global monetary policy which aims to dampen demand to such a degree that price setters have no choice but to lower prices. However, in the presence of suborn inflation like we are witnessing now, there is always a risk of overtightening which can plunge an economy into a recession.

Technical recessions have carried less weight this time around due to historically high labour markets and besides, the US emerged from a technical recession in 2022 only to post a 3.2% rise in GDP growth the very next quarter. However, declining GDP growth indicates a deteriorating macroeconomic environment in which German companies could face further challenges.

ECB Talks Tough on Inflation but Nears Peak Rates

Reaching peak rates is fully dependent on the predictability of disinflationary trends. If core inflation in the euro area drops steadily, then the ECB can look to pause. If core inflation behaves in a manner similar to the what’s been seen in the UK with subsequent upward revisions, then will have to continue higher. Tightening the screws in an economy that is already showing signs of distress isn’t ideal, which is why the ECB is hoping that prior hikes will have the desired effects on inflation. ECB members have hinted at another 25-bps hike in Q3 with potentially one more before interest rates are broadly seen as sufficiently restrictive. Markets concur, pricing in just under 50bps more to come, leaving rates at 4% potentially.

Market Implied Rates into Year End

Source: Refinitiv

Bear in mind, the ECB announced an end to all Asset Purchase Programme (APP) reinvestments from July which ought to remove liquidity from financial markets. The overall effect of this move on liquidity is uncertain given that reinvestments of maturing securities under the Pandemic Emergency Purchase Plan (PEPP) are still set to continue and until the end of 2024. Nevertheless, the decision does imply further tightening of financial conditions.

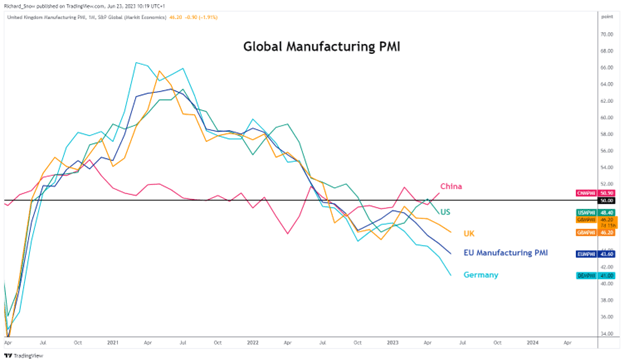

German & EU Manufacturing Leads the Pack Lower

Deteriorating data continues to emerge as EU and German manufacturing PMI data dropped more than expected in June. This has negative ramifications for the relative services sectors as the manufacturing trends typically lead the services sector. Services, up until recently, had shown a resilience but with lower-than-expected prints filtering in, it would appear that the direction of travel has already been predetermined.

Germany Leading the Global Downtrend in Manufacturing PMI (S&P Global)

Source: TradingView

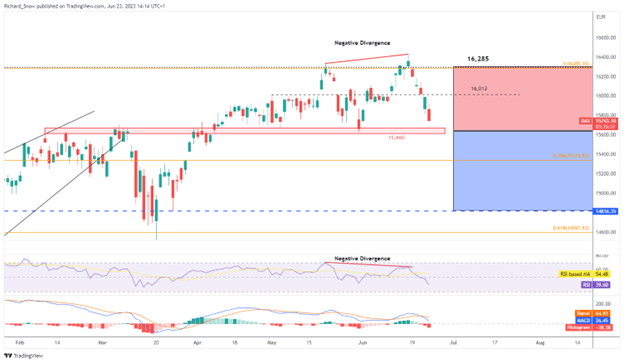

DAX Warning Signals Flash Red at the End of Q2

The German index traded towards the underside of the ascending channel in the latter stages of Q2 as economic data showed signs of worsening. Forecasting around the end of a tightening cycle is a tricky task as inflation tends not to decline in a straight line, meaning markets can be prone to extended periods of up and down price action without settling on a direction.

Nevertheless, if the economic headwinds accrue, The DAX could move lower in the third quarter of the year. The move however would be contingent upon a move and close below 15,660 on the weekly chart which ought to coincide with a breakdown of the ascending channel. 15,660 signifies a level of interest that has acted as support and resistance previously. The 3-month average true range comes in around 800 points meaning that a bearish continuation highlights 15,070 on the way to 14,815.

Should prices continue higher, resistance of 16,290 can be seen as the invalidation level of the bearish setup, ahead of the all-time high of 16,427.

Weekly DAX Chart

Source: TradingView

Recommended by Richard Snow

See what other Q3 trades have been identified by analysts

The daily chart helps to show the waning momentum in the lead up to the start of Q3 as price action printed a higher high but failed to do so on the RSI – something referred to as negative divergence. It implies that bullish momentum is slowing down which can point to a reversal further down the line.

Daily DAX Chart

Source: TradingView

Comments are closed.