Fed-BoJ policy divergence remains the key driving force

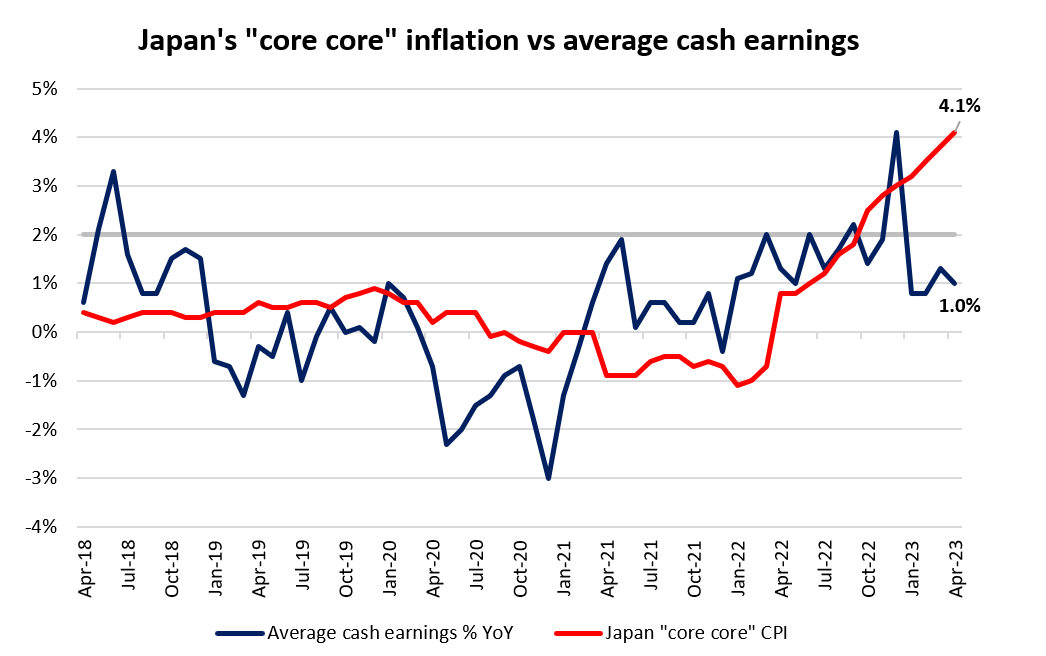

While the Federal Reserve (Fed) has largely retained its hawkish tone at the latest meeting, speculations for a quicker policy shift from the Bank of Japan (BoJ) have not been receiving much validation by policymakers thus far. The persistent rise in Japan’s “core core” inflation to more than two-fold the central bank’s target (4.1% versus 2% target) has been an argument from the hawks but considering that improving wage dynamics has not been broad-based, that has provided some basis for the BoJ to continue defending their stance of inflation being ‘transitory’.

Source: Refinitiv

Current interest rate futures remain well-anchored for the BoJ to leave interest rate unchanged at least over the next two policy meetings. Perhaps the greater focus will be on whether the central bank will exercise further tweaks to its yield curve control (YCC) policy, as markets have been highly sensitive to any slightest signs of policy normalisation from the central bank.

That said, the BoJ has not been the best at communications. One may recall how the central bank threw markets off guard back in December 2022 with a surprise widening of its 10-year bond yield cap, dragging the USD/JPY down by 4.3% in a single day. With the still-ambiguous outlook on how the BoJ may normalise policies eventually, any tweaks will continue to come with an element of surprise. At least for now, the tone from the central bank seems to be pointing to more wait-and-see, which provides some runway for the Fed-BoJ policy divergence story to continue.

How did past BoJ’s intervention play out?

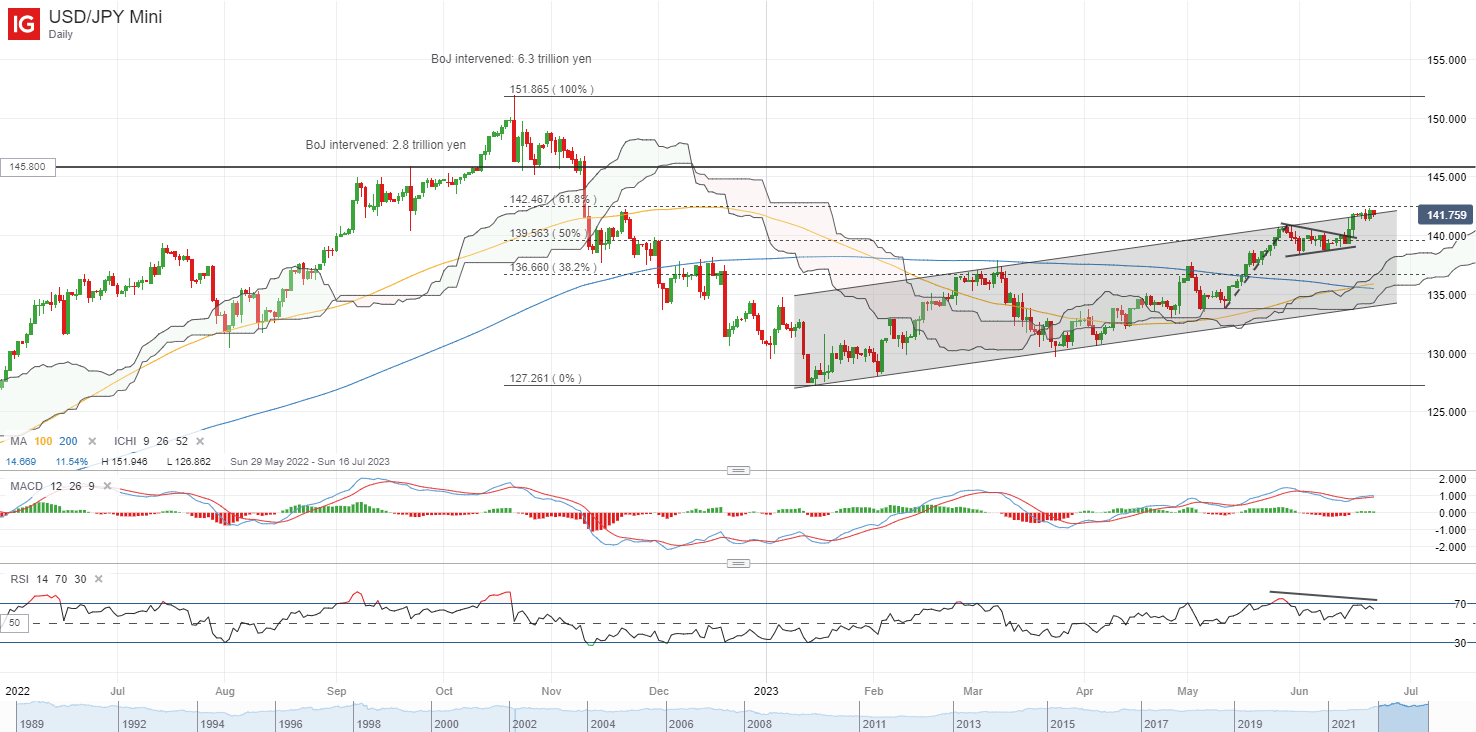

The BoJ has intervened in the currency market thrice last year, once in September 2022 by buying 2.8 trillion yen while selling the US dollar. The second and third occasions are on 21 and 24 October 2022, with an overall 6.3 trillion yen amount. While the October intervention has allowed the USD/JPY to find a top, recent resurgences in the pair seems to suggest that as long as the policy divergence remains, any impact from interventions could be temporary and unsustainable over the longer run.

Thus far, policymakers’ concerns on the weaker yen have not been as prominent as it was last year. Recent comments from the BOJ Governor Kazuo Ueda also highlighted that focus is on the pace and timing of decline as compared to an absolute level, which may point to some acceptance for now.

Technical analysis: USD/JPY closing in on BoJ intervention level back in September 2022

On the daily chart, the USD/JPY has been trading within a rising channel pattern since the start of the year, with a bullish crossover formed between its 100-day and 200-day moving average (MA). Despite the recent lacklustre performance in the US dollar, the pair has managed to hold up well, as the Fed-BoJ policy divergence remains the key driver. A bullish pennant has been presented lately, although in the near term, some indecision seems to be in place with a bearish divergence on the relative strength index (RSI).

While the series of higher highs and higher lows continue to put an upward trend in place, immediate resistance may stand at the upper channel trendline, in coincidence with a 61.8% Fibonacci retracement level. Any upward break above the channel pattern may then leave the 145.80 level on watch next. To recall, the BoJ has intervened in the currency market at this level back in 22 September 2022, which could trigger concerns that the BoJ may step in once more.

Source: IG charts

Comments are closed.