We’re about to see Uncle Sam’s July inflation data!

Are consumer prices decelerating quickly enough to discourage more rate hikes from the Fed?

Here are points you need to know if you’re trading Wednesday’s event:

Event in Focus:

U.S. headline and core CPI readings for July 2023

When Will it Be Released:

August 10, 2023 (Thursday), 12:30 pm GMT

Use our Forex Market Hours tool to convert GMT to your local time zone.

Expectations:

- U.S. headline consumer price index m/m: maintain June’s 0.2% growth

- U.S. headline consumer price index y/y: 3.3% forecast vs. 3.0% previous

- U.S. core consumer price index m/m: maintain June’s 0.2% growth

- U.S. core consumer price index y/y: maintain June’s 4.8% growth

Relevant Data Since Last Event/Data Release:

🟢 Arguments for Strong Inflation Update / Likely Bullish USD

Preliminary Consumer Sentiment for July: 72.6 (64.5 forecast; 64.4 previous); short-term inflation expectations ticked up from 3.3% to 3.4%

Flash Composite PMI: “The rate of increase in total input prices softened in July to the slowest since October 2020” but the rate of output charge “picked up” as firms passed through higher costs and interest payments to customers.

FHFA House Price Index in May: 0.7% (0.5% m/m forecast; 0.7% previous)

CB Consumer Confidence Index for July rose to 117.0, the highest level since July 2021

University of Michigan Consumer Sentiment Index for July: 71.6 vs. 64.4 previous

JOLTS Job Cuts in July: 23.6K vs. 40.7K cuts in June

Non-Farm Payrolls for July: 187.0k (190.0k forecast; 185.0k previous); Unemployment rate dipped to 3.5% (3.6% forecast/previous); Average hourly earnings steady at 0.4% m/m (vs. 0.3% expected)

ISM July Services PMI price index is up by 2.7 pts to 56.8 (vs. 54.1 previous)

S&P Global Services PMI price index: “Input costs at service providers increased at a further marked pace during July… Selling prices continued to rise at a pace that was faster than the series trend.“

🔴 Arguments for Weak Inflation Update / Likely Bearish USD

Existing Home Sales for June: -3.3% m/m (-1.2% m/m forecast; 0.2% m/m previous); the downturn is mainly due to extremely low inventory of pre-owned homes

Weekly jobless claims rose by 6k w/w to 227k; unit labor costs rose by 1.6% q/q vs. 4.2% q/q/ previous

Previous Releases and Risk Environment Influence on the U.S. Dollar

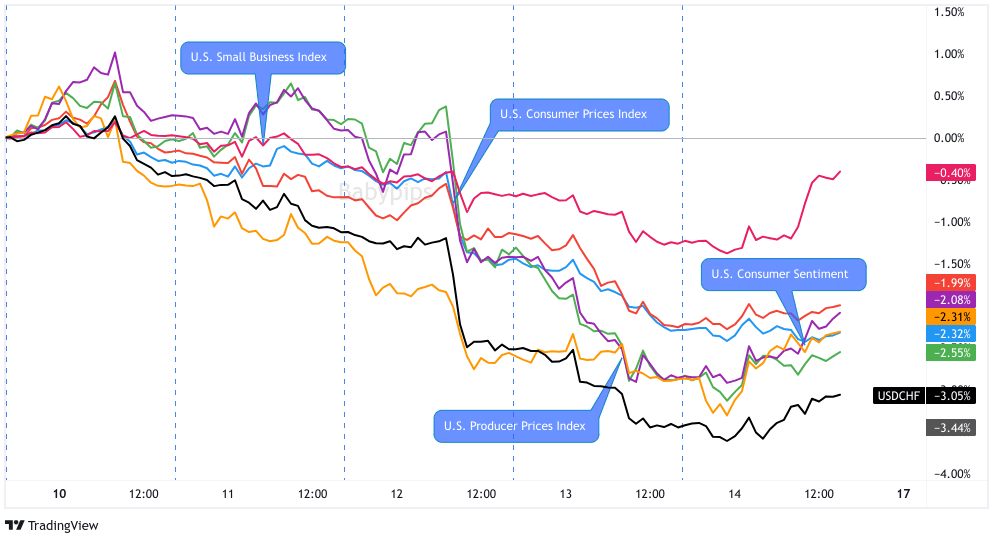

July 12, 2023

Overlay of USD vs. Major Currencies Chart by TV

Event results / Price Action:

June’s CPI numbers confirmed a further slowdown in consumer prices, with the headline CPI showing a monthly growth of 0.2% (vs. 0.3% expected) and annual growth of 3.0% (down from 4.0% and much closer to the Fed’s 2.0% target).

The U.S. dollar, which had been losing ground earlier in the week over risk-taking and slower inflation bets, accelerated its downswings and made new intraday and intraweek lows by the end of the trading session.

Risk environment and intermarket behaviors:

Speculation of weaker U.S. inflation and downbeat Chinese data got traders pricing in governments stepping in with stimulus. Specifically, they were betting on the Fed postponing its rate hike and the Chinese government announcing a fresh set of government stimulus measures.

Traders started buying “risk” assets on Monday’s U.S. session trading and the U.S. CPI release accelerated the week’s risk-friendly trends. The safe havens eventually found intraweek bottoms a day after the inflation report on Thursday.

June 13, 2023

Event results / Price Action:

Headline CPI for May missed the mark, coming in at 4.0% year-over-year versus estimates of a drop from 4.9% to 4.3%. The core version of the report also tumbled from 5.5% year-over-year in April to 5.3% in May.

As a result, the Greenback gave up most of its gains from earlier in the week, as traders adjusted bets for a likely Fed pause.

The FOMC kept rates unchanged as expected but signaled that two more hikes could be on the horizon, allowing the dollar to pull up from its drop later on. However, another batch of mostly downbeat data forced the U.S. currency to resume the slide on Friday.

Risk environment and intermarket behaviors:

Traders seemed to be on edge early in the week, as the schedule was filled with top-tier releases and central bank decisions.

Risk-on flows picked up when the PBOC surprised the markets with their decision to cut the 7-day reverse repo rate from 2.0% to 1.9% and lower the onshore reference rate by 200 points.

Safe havens gave up more ground when market players got wind of downbeat data from China, as these boosted hopes for more stimulus.

Price action probabilities:

Risk sentiment probabilities:

Risk takers are walking on eggshells as they price in China’s weak trade data and ratings agency Moody’s downgrading 10 U.S. banks and reviewing other (bigger) banks.

It also doesn’t help that Italy approved an unexpected 40% windfall tax on Italian banks’ “surplus profits” from the rise of interest rates.

Safe havens like government bonds and USD and CHF are trading higher while “risky” bets like crude oil and commodity-related currencies are trading lower.

The next broad risk sentiment catalyst ahead of the U.S. CPI event is likely China’s inflation update, with expectations of negative annualized inflation rates for both CPI and PPI. This can go either way for risk sentiment as falling inflation is a signal of weakening economic conditions in the second largest economy in the world, but it may also spark action from the Chinese government to stimulate the economy.

Keep a close eye on this event and the market reaction to gauge risk sentiment going into the U.S. CPI event.

U.S. Dollar scenarios:

Potential Base Scenario:

Based on the indicators above, Americans are still finding jobs and turning more confident while prices continue to rise.

Aside from the expected uptick in the annual rate due to base year adjustments, we could see the monthly headline and core CPI maintain their 0.2% growth rate. Steady or faster price increases may be enough to keep the September rate hike bets alive.

In this scenario, look out for potential long USD plays against commodity-related currencies, particularly AUD, NZD, and CAD since they in momentum mode from China’s weak trade data. Comdoll selloffs might even be extended for the rest of the week if risk aversion remains in play.

Potential Alternative Scenario:

If consumer prices rise slower than markets are expecting, then the Fed will have more room to keep its interest rates steady for longer.

In this scenario, risk-taking could pick up and push “riskier” bets like the comdolls, crude oil, and cryptocurrencies and drag the U.S. dollar lower. Of course, the volatility of the anti-USD reaction will also depend on the overall market sentiment.

Unless we see other market-moving catalysts, any reports that support further interest rate hikes may extend this week’s risk-averse trading environment and limit USD’s losses.

And keep in mind for both scenarios, the U.S. dollar has been in rally mode this week, and if it continues to run higher into the event, the odds rise of a “buy-the-rumor, sell-the-news” scenario playing out. It’s something to consider and it may be a good idea to wait-and-see the numbers/reaction before building out a risk management plan.

This content is strictly for informational purposes only and does not constitute as investment advice. Trading any financial market involves risk. Please read our Risk Disclosure to make sure you understand the risks involved.

Comments are closed.