Uncle Sam has another batch of inflation figures comin’ right up!

Can these still make or break Fed tightening expectations? And how might the U.S. dollar react to the actual results?

Here’s what market watchers are expecting for the U.S. August CPI report.

Event in Focus:

U.S. headline and core CPI readings for August 2023

When Will it Be Released:

September 13, 2023 (Wednesday), 12:30 pm GMT

Use our Forex Market Hours tool to convert GMT to your local time zone.

Expectations:

- U.S. headline consumer price index m/m: +0.6% forecast vs. +0.2% previous

- U.S. headline consumer price index y/y: +3.6% forecast vs. +3.2% previous

- U.S. core consumer price index m/m: +0.2% forecast vs. +0.2% previous

Relevant Data Since Last Event/Data Release:

🟢 Arguments for Strong Inflation Update / Likely Bullish USD

August ISM services PMI prices component rose 2.1 points to 58.9 to indicate faster pace of gains

August S&P Global manufacturing PMI: “Average input prices rose for the second month running, and at a slightly faster rate… Higher costs continued to be passed on to customers, as output prices rose at the fastest pace in four months albeit a pace that remained modest overall.”

July headline and core PPI rose 0.3% m/m vs. estimated 0.2% upticks

🔴 Arguments for Weak Inflation Update / Likely Bearish USD

August ISM manufacturing PMI prices component rose 5.8 points from July’2 42.6 reading to 48.4 to reflect slower pace of declines

August S&P Global services PMI: “Input prices rose at a steeper pace in August, which was largely driven by higher wage bills. Firms were hesitant to pass through the full extent of increased input prices to their clients, however, as selling prices rose at a softer pace.”

Average hourly earnings slowed from a 0.4% m/m gain in July to a meager 0.2% uptick in August

Previous Releases and Risk Environment Influence on the U.S. Dollar

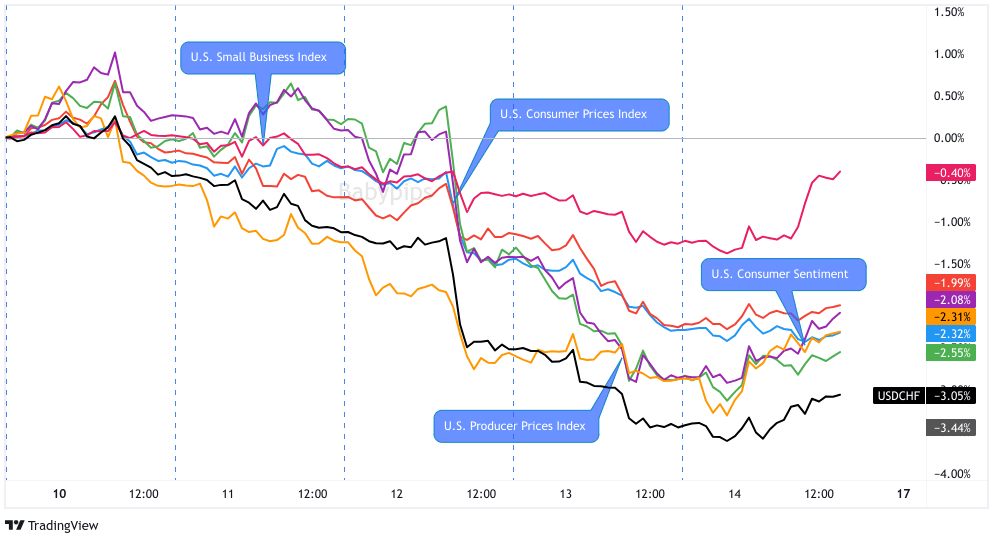

August 10, 2023

Event results / Price Action:

The July CPI report came in mostly in line with market estimates of 0.2% gains for both headline and core figures, but the year-over-year figure fell short at 3.2% versus the projected 3.3% reading.

The Greenback was off to a shaky start for the week as traders tried to gauge how the actual inflation figures might turn out. Fortunately risk-off flows came in play and kept the safe-haven dollar supported early on.

Hawkish Fed commentary and an upbeat PPI report helped the U.S. currency extend its rally until the end of the week.

Risk environment and intermarket behaviors:

Downbeat Chinese trade and inflation data printed at the start of the week helped buoy the safe-haven dollar higher against most of its rivals, even after jitters about a potential September government shutdown hit the airwaves.

The dollar also got an extra boost from reports of an increased Treasury supply, as the auction of 30-year bonds was awarded at higher-than-expected yields and the amount allotted to primary dealers was the highest since February.

July 12, 2023

Overlay of USD vs. Major Currencies Chart by TV

Event results / Price Action:

The June CPI report confirmed a slowdown in price pressures, as the headline reading came in at 0.2% versus the estimated 0.3% month-over-month growth. This brought the annual CPI down from 4.0% to 3.0% for the period.

These were enough to weigh on Fed tightening hopes in the coming months, accelerating the dollar selloff that started much earlier in the week.

Another wave lower ensued after the PPI readings were printed the next day, as lower than expected producer price gains pointed to consumer inflation slowing much further in the coming months.

Risk environment and intermarket behaviors:

Risk appetite was in play at the beginning of the week, as traders had been anticipating stimulus efforts from China, as well as dampened rate hike expectations due to potentially weak U.S. CPI.

Commodities and equities were on strong footing for the most part of the week, leading traders to keep dumping their safe-haven holdings. Treasury yields carried on with their slide, as markets started pricing a Fed funds rate of 3.71% by December 2024, down from the 4.10% forecast earlier in the week.

Price action probabilities:

Risk sentiment probabilities:

Dollar domination was the main theme for the previous trading week, as mostly upbeat data and hawkish rhetoric lifted Fed rate hike hopes for this month.

As a result, risk assets like commodities and equities could keep shedding gains, especially if the prospect of higher borrowing costs keep recession jitters in play.

Also keep in mind that the likes of the RBA and BOC recently decided to sit on their hands during their latest policy decisions, leaving the Fed as probably the most hawkish central bank out there.

Looking forward, broad risk sentiment around the U.S. CPI release will likely continue to lean slightly risk-off, but Dollar sentiment may influence that a bit as traders will likely take off some risk / profits after last week’s strong Dollar run.

We’ll also be getting mid-tier economic updates from around the world, most notably U.K. jobs & GDP, as well as Germany economic sentiment data. If they both point to weakening conditions, that may also contribute to a bearish lean heading into the Wednesday U.S. trading session.

U.S. Dollar scenarios:

Potential Base Scenario:

Leading indicators are showing evidence of another pickup in input prices but that businesses are hesitant to pass on these costs to consumers. Wage inflation appears to be slowing as well.

With that, the August CPI report may still reflect subdued consumer inflationary pressures but not enough to derail September FOMC tightening expectations. A stronger-than-expected read might even spur rate hike hopes in the coming months.

If that’s the case, the U.S. currency could strongly benefit from both fundamentals and market sentiment. After all, the possibility of seeing higher U.S. borrowing costs could keep traders on edge about a slowdown in global growth.

In this scenario, look out for opportunities to buy the dollar against higher-yielding currencies like AUD, NZD, and CAD, especially since their central banks have just shifted to a more cautious stance.

Equity indices and commodities might be worth checking out for short setups against the Greenback as well, although gold might bust out its safe-haven moves if recession fears kick into high gear.

Potential Alternative Scenario:

A significant downside surprise in the August CPI report may give dollar bulls further reason to pause, rethink , and potentially reduce their September rate hike bets.

Either that or market participants could go for a “buy the rumor, sell the news” scenario if the actual results fail to impress. After all, September tightening hopes have been priced in for quite some time, so any hints that future rate hikes are off the table could spur profit-taking off the recent USD rallies.

Comments are closed.