Can you believe it’s almost time for another RBA statement?!

If you’re planning on trading this top-tier event, better read up on what analysts are expecting for the September decision.

Event in Focus:

Reserve Bank of Australia (RBA) Monetary Policy Statement

When Will it Be Released:

September 5, 2023 (Tuesday): 4:30 am GMT

Use our Forex Market Hours tool to convert GMT to your local time zone.

Expectations:

- RBA to keep its interest rates steady at 4.10% for the fourth month in a row in September

- RBA’s statement may emphasize the need for further tightening under the appropriate conditions

Relevant Australian Data Since the Last RBA Statement:

🟢 Arguments for Tighter Monetary Policy / Bullish AUD

Retail sales rose by 0.5% m/m in July vs. estimated 0.2% uptick and earlier 0.8% slump

🔴 Arguments for Looser Monetary Policy / Bearish AUD

Headline CPI slowed from 5.4% year-over-year in July to 4.9% vs. estimated dip to 5.2%

July employment change showed 14.6K decline in hiring vs. estimated 14.6K increase and earlier 31.6K gain, jobless rate ticked up from 3.5% to 3.7% vs. 3.6% forecast

Wage price index increased by another 0.8% in Q2 vs. estimated 0.9% gain, up 3.6% year-over-year

Previous Releases and Risk Environment Influence on AUD

August 1, 2023

Action/results: Aussie bulls were eager to charge this week in anticipation of another RBA interest rate hike. However, the central bank surprised the markets by keeping rates on hold at 4.10% instead of increasing to 4.35%.

In addition, policymakers set the expectation that while open to further hikes, future decisions will be data dependent. This set off a steady AUD downtrend that lasted for the most part of the week, before market players booked profits ahead of NFP Friday.

Risk environment and Intermarket behaviors: Rumors that the Chinese government is gearing up for a massive batch of stimulus efforts sparked a risk-on rally at the beginning of the trading week.

The tide turned when China printed a downbeat manufacturing PMI which reflected a shift to industry contraction, triggering a selloff for risk assets like commodities.

This was followed by Fitch’s credit rating downgrade on the U.S. over the economy’s growing debt levels, extending risk aversion’s stay in the markets.

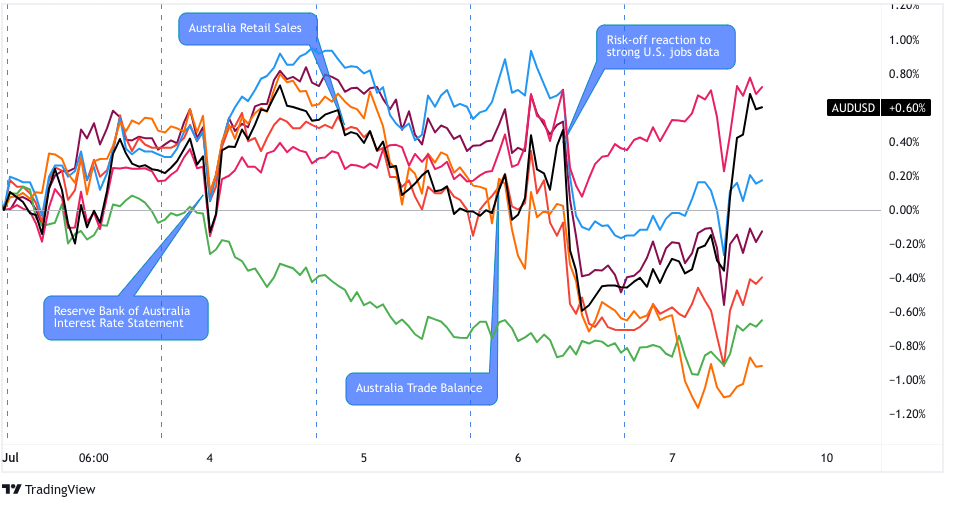

July 4, 2023

Overlay of AUD vs. Major Currencies Chart by TV

Action/results: The Australian central bank decided to keep rates on hold, disappointing those who had projected another hike in borrowing costs.

In the accompanying statement, policymakers noted that inflation has “passed its peak” but that “some further tightening” may still be required.

Not surprisingly, the Aussie took major hits when the announcement was made, although the “hawkish pause” allowed the commodity currency to recoup its losses by the end of the day.

Risk environment and Intermarket behaviors: Risk-off flows greeted market players on Monday, following surprise output cuts from Russia and Saudi Arabia plus weak PMI reports from the U.S. and China.

There wasn’t much to go on for the rest of the week in terms of economic data, and the U.S. holiday on Tuesday kept liquidity capped. With that, risk aversion stayed in play for the most part of the week, especially after the FOMC minutes pointed to the possibility of even more interest rate hikes.

Price action probabilities

Risk sentiment probabilities: Risk sentiment ahead of the RBA decision on Tuesday may take cues from China’s Caixin services PMI, which may continue to weaken from its 2023 peak of 57.8 back in March. On one hand, a weaker read may draw in recession wary traders, which may spark stronger calls for more stimulus from the government and central bank.

That latter doesn’t always materialize after fresh weak economic updates from China, so it’s likely the best practice to see what China Services PMI gives us and the market reaction before taking a risk sentiment lean.

Australian Dollar scenarios

Base case: The latest batch of economic data from the Land Down Under is pointing to low odds of an interest rate hike from the RBA this time around.

In particular, inflation-related reports such as the CPI, PPI, and wage price index are reflecting subdued price pressures, which means that the central bank is more than likely to be in no rush to resume tightening.

Besides, mostly downbeat PMI readings from China, Australia’s top trade partner, could also be indicative of slower commodity exports.

Highlighting these points could lead AUD traders to believe that the RBA would sit on its hands for much longer, possibly triggering losses against currencies with central banks that are still open to hiking, such as the BOE and Fed.

The odds of a bearish reaction in AUD rises if we see AUD make gains in the U.S. session ahead of the event release, and IF China Services PMI data disappoints and we see no support action / announcements on the session.

Alternative Scenario: Although the RBA is likely to stand pat in September, announcing a “hawkish hold” may bring some upside for the currency.

In particular, policymakers could point to the rebound in business and consumer spending, which might then translate to a recovery in the labor market and wage inflation later on.

In this very low probability (but not non-zero) scenario, the possibility of further tightening down the line could be enough to get AUD bulls charging short-term against currencies with more dovish central banks, like the BOJ, especially if risk sentiment is leaning positive on the session.

Comments are closed.