Dow, Nasdaq 100, Dollar, USDJPY and Rate Forecasts Talking Points:

- The Market Perspective: USDJPY Bullish Above 132.00; EURUSD Bearish Below 108

- In a week packed with event risk, the strong US NFPs and service sector activity shaped the Fed rate hike interpretation for a distinct Dollar take

- Where the Greenback’s fundamentals seem more direct, the bearings for risk trends as the Dow broods and Nasdaq jumps around are unresolved

Recommended by John Kicklighter

Get Your Free Top Trading Opportunities Forecast

As we look ahead to a new trading week, what is the background mood of the market? An argument can be made by the bulls who point to the general progress made by benchmarks like the Nasdaq 100 over the entirety of this past week – a general push to four-month highs – with justification developed around an impending peak in the major central banks’ tightening cycle and improvement in growth forecasts. Alternatively, bears can draw on the late retreat Friday from the same measures with backing through the erosion of terminal rate discounts. However, these are debate points founded more on belief than tangibility. That means that the ultimate bearing the market takes will be highly contentious and founded more on the collective speculative view and less on scheduled developments.

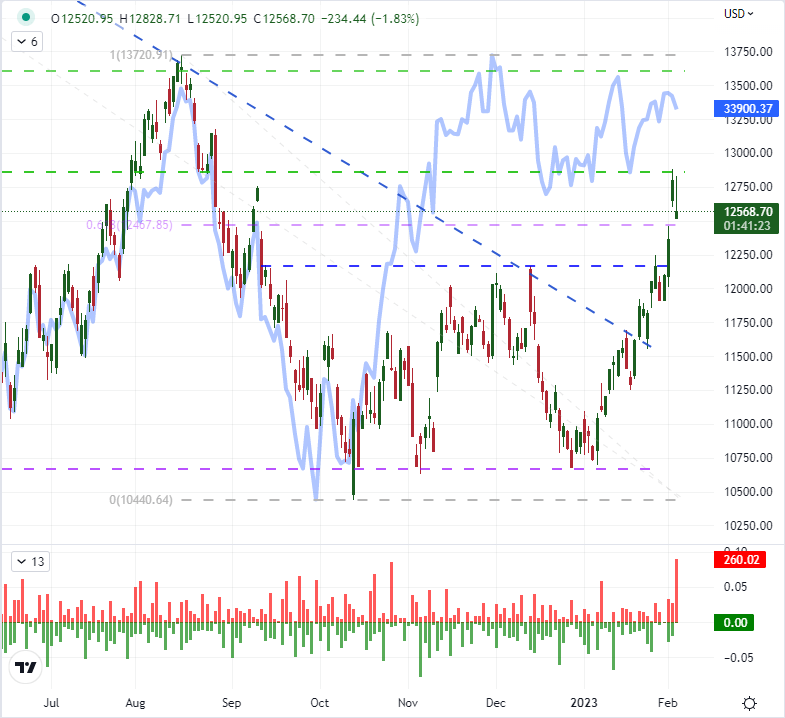

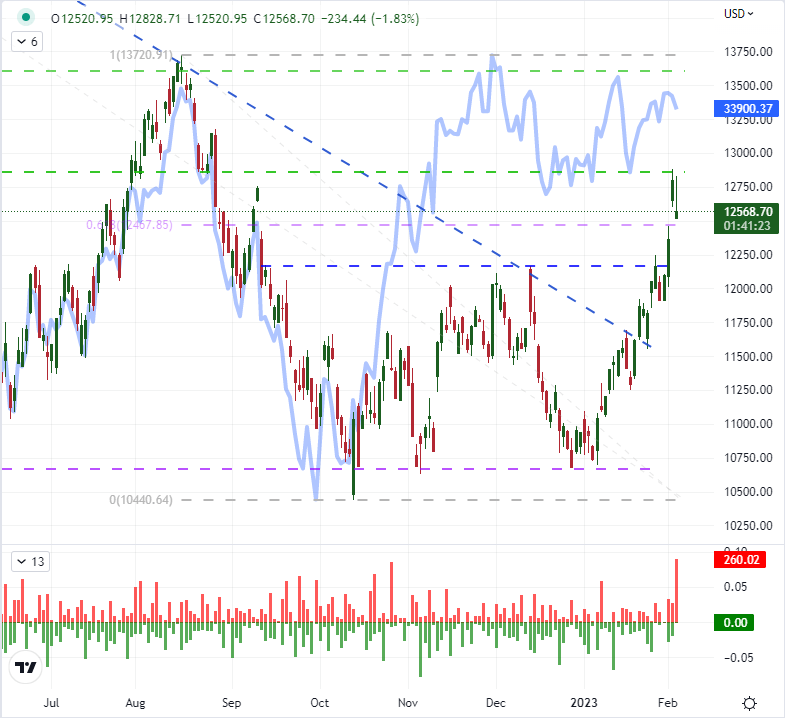

I long ago resolved myself to the reality that the communal view of the market is what ultimately directs price action. As the saying goes, the ‘market can remain irrational longer than you can solvent’; but the perception of irrationality is itself judgement. That said, there are some underlying aspects to the market that I believe will factor into the overwhelming current of sentiment. The Dow Jones Industrial Average’s refusal to participate in the swell of enthusiasm is remarkable. It wasn’t the only ‘risk’ connected asset not to take part, but the disparity between the Dow (‘value index’) and Nasdaq 100 (‘growth index’) was striking. It perhaps is a result of a resurgence in speculative participation relative to larger market players. The former typically holds a shorter duration and acts on more unconventional reasoning. The latter is more often the foundation for trend development. How can we distinguish market groups? Beyond comparison of close counterparts like Dow-NDX, options activity of retail traders (as a percentage of the entire market) surged to overtake the ‘meme stock’ craze peak this past week.

| Change in | Longs | Shorts | OI |

| Daily | -9% | 0% | -4% |

| Weekly | 4% | -8% | -4% |

Chart of Dow Jones Industrial Average and ‘Wicks’, Overlaid with the Nasdaq 100 (Daily)

Chart Created on Tradingview Platform

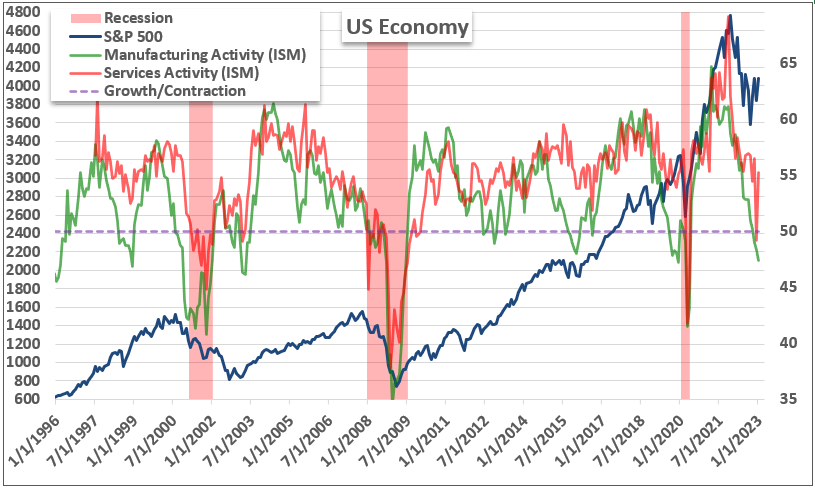

Looking out over next week’s fundamental docket, there is nothing of prominence that would readily be considered capable of redefining broader risk trends – not like the FOMC decision or NFPs that we had this past week. That means that the winds already to our back will converge with unpredictable headlines and organic speculative trends to form whatever systemic trends we ultimately find. For the current fundamental mix, two major events on Friday seemed to materially change the tone of speculation. After the Federal Reserve’s decision this past Wednesday to hike rates 25 basis points and offer rhetoric to suggest it was still on pace for its projected terminal rate, the market was happy to once again discount the authority’s forecast. That changed, however, when the ISM services report for January was released. The world’s largest economy is heavily dependent on service-based businesses for growth and employment, and the past month’s measure jumped much more sharply than expected – alleviating much of the concern of recession associated to the previous month’s surprise slump (below 50.0). While that can be a boon for growth potential, it is also a capital market burden in supporting the Fed’s drive.

Chart of S&P 500 with US Mfg and Service Activity, Overlaid with Official Recessions (Monthly)

Chart Created by John Kicklighter

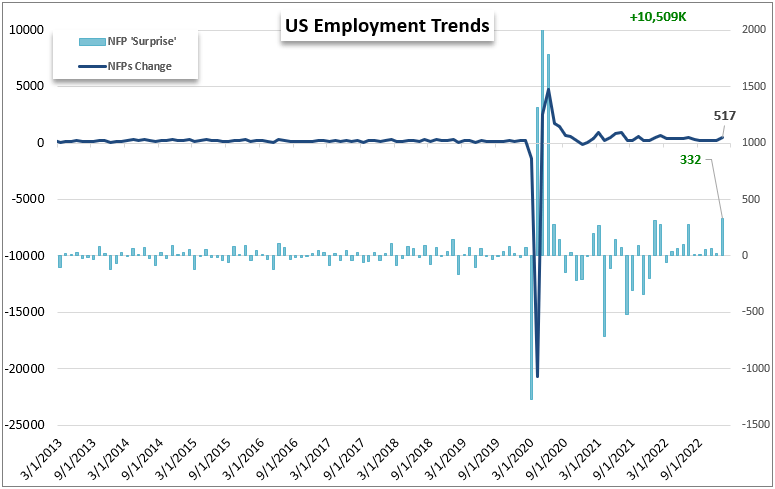

The prop to Fed forecasts was even more distinctly bolstered by the January labor report. Nonfarm payrolls (NFPs) increased by a net 517,000 which was substantially higher (by 332,000 positions) than the economist consensus. With average hourly earnings growing another 0.3 percent and the jobless rate dropping to a seven decade low, there was a clear divergence in the focus of the central bank’s dual mandate for full employment and stable inflation.

Chart of US Change in Nonfarm Payrolls with Level of ‘Surprise’ Relative to Forecasts (Monthly)

Chart Created by John Kicklighter

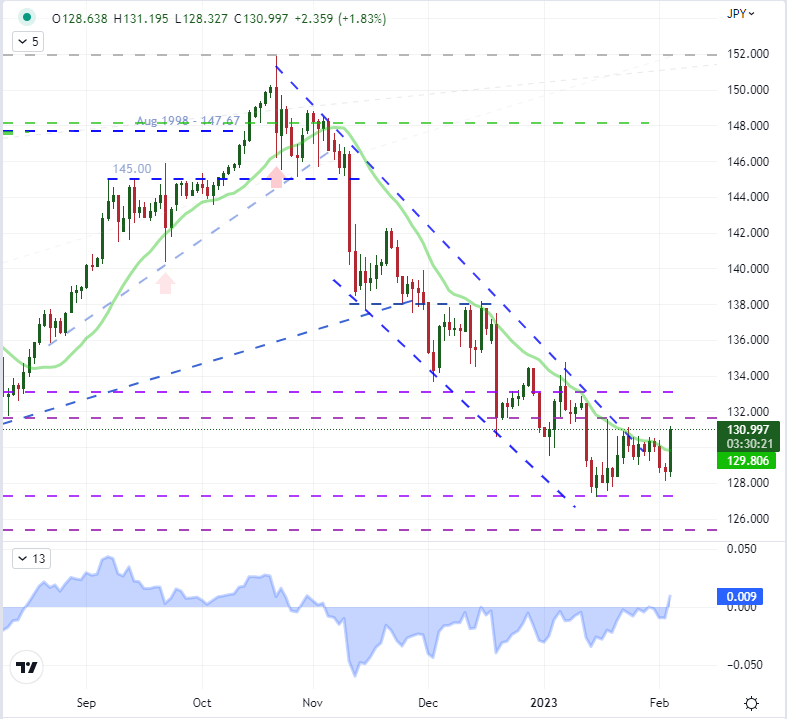

There were some remarkable moves to come out of this fundamental mix outside of the US indices. In single shares, the top tech stocks which reported earnings after the close Thursday found Google and Amazon sporting serious reversals while top market cap company Apple weathered the storm with a 2.4 percent gain. US 2-year yields charged 19 basis points higher while gold suffered its biggest drop in six months. From the Dollar, there was a notable rally registered across the spectrum as rate forecasts climbed. From a technical perspective, EURUSD through its break of the rising wedge from November and the 20-day moving average. That said, its fundamental backdrop is not as steady. While the Dollar is looking to maintain a yield advantage through their respective terminal rates, the ECB peak is still ambiguous. USDJPY on the other hand is fairly clear with its yield focus on the US side of the equation (though it is an outlier risk the BOJ surprises again like December). What’s more, this pair is also better aligned to risk trends. Looking into next week, it is possible that ‘risk appetite’ is restored but given we are already buoyant on that front with VIX very low, that development would likely be choppy with limited stretch. A spell of fear on the other hand could come swiftly and exact a serious toll. While we often treat the Yen as a ‘haven’; with USDJPY, there is a positive correlation to the VIX.

| Change in | Longs | Shorts | OI |

| Daily | -26% | 10% | -8% |

| Weekly | -12% | -3% | -7% |

Chart of USDJPY with 20-Day SMA and Spot-20SMA Disparity (Daily)

Chart Created on Tradingview Platform

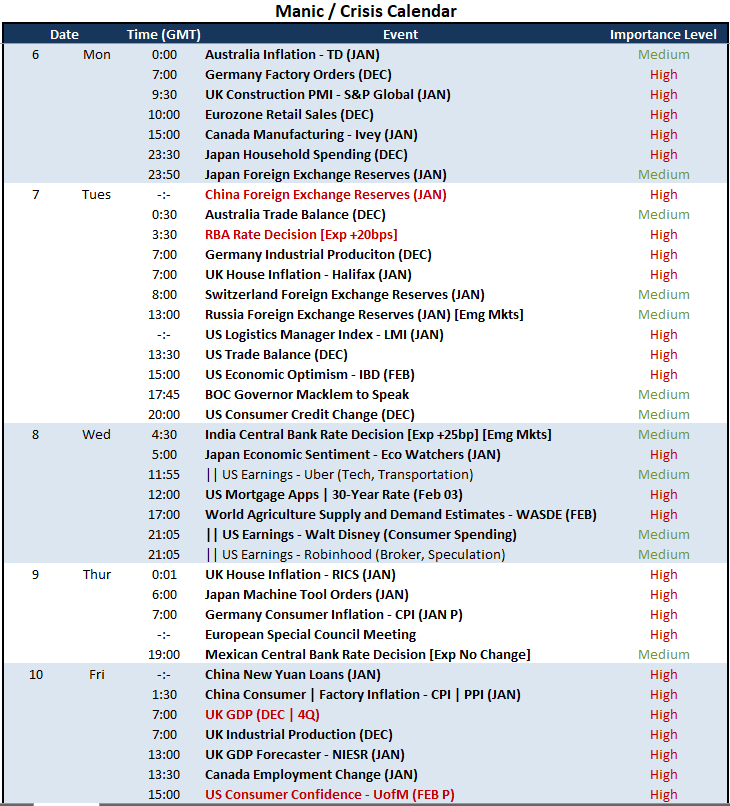

While the forthcoming economic docket doesn’t offer much in the way of systemic guidance for the global capital markets, there are nevertheless events for which we should keep track. Monetary policy will likely manifest in more relative consideration rather than a collective perspective (unless sentiment sours). With that said, central bank speak will be a moving target while the Reserve Bank of Australia (RBA) decision will offer the only update from a major player. With AUDUSD dropping, a dovish outlook after an expected hike could exacerbate the rebalance. On the growth / recession side of the conversation, there are secondary indicators galore such as Canadian manufacturing, German industrial production, US economic sentiment and Japanese household spending. Standouts will be Chinese foreign exchange reserves, UK GDP and US consumer sentiment (from the UofM).

Top Global Macro Economic Event Risk for Next Week

Calendar Created by John Kicklighter

Discover what kind of forex trader you are

Comments are closed.