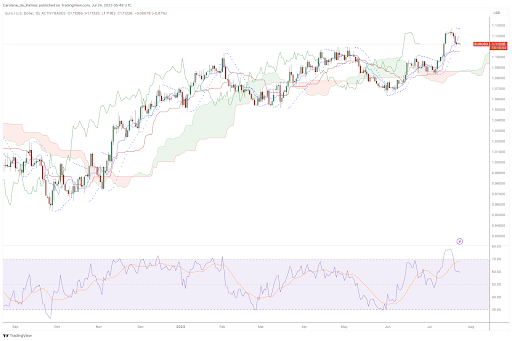

Between July 6th and July 17th, the EUR/USD showed a remarkable upward trend, soaring from 1.08536 to 1.12484.

Yet, the tides have shifted since then, as the pair embarked on a correction phase, experiencing a decline of around 1%.

As forex traders gear up for what promises to be a busy week ahead, the EUR/USD is currently trading at 1.11221, leaving market participants eagerly awaiting new developments from the Fed and the ECB.

Daily EUR/USD Chart – Source: ActivTrader’s data on TradingView

A crucial week for the EUR/USD

The week ahead promises to be a significant one for economic and financial news all across the globe.

In the midst of a whole host of major companies posting their second-quarter earnings, some of the largest central banks, including the European Central Bank and the Federal Reserve, are also set to meet on the direction of their country’s interest rates.

After a prolonged period in which the US dollar gained ground against other major currencies resulting from faster monetary tightening in the US than elsewhere, the dollar has been steadily declining.

After the most recent inflation report, it reached its lowest level in more than 15 months.

Daily US Dollar Index Chart – Source: TradingView

This underscores optimism that the Fed’s monetary tightening is possibly nearing its end, even while it continues in Europe and other places. This in turn translates into stronger international profits for US businesses, less debtor pressure in emerging markets, and higher local currency earnings for countries that export raw materials.

Below we’ll cover what to expect from the ECB and Fed meetings based on some of the latest data, and what impact it may have on the direction of the EUR/USD.

Fed Monetary Policy Meeting

Wednesday, July 26th. Decision at 6:00 PM GMT

After holding interest rates stable for the first time in 15 months in June, officials on the FOMC don’t seem to want to wait too long to resume the tightening cycle. Expectations are for the committee to raise rates again this week, marking the eleventh overall hike since March 2022.

The debate amongst economists and investors at current is whether or not more rate rises are really required to guarantee that inflation drops low enough to remain stable, or whether or not doing more may cause undue harm to the economy if it were implemented.

The annual inflation rate in the US fell a decent amount from 4% to 3% in June, the lowest since March 2021. The core rate also fell to 4.8%, its lowest level since October 2021.

Also in May, the US personal consumption expenditure price index grew 3.8% year on year, the lowest figure since April 2021, compared to a downwardly revised 4.3% growth in April. Progress like this might leave some to wonder if it will continue to improve on its own without further intervention.

Whether or not the Fed will continue to tighten policy is heavily dependent on the reaction of the labor market too. Americans’ ability to keep spending thanks to the robust employment market is bolstered by their optimism about the economy’s long-term prospects, which in turn encourages them to keep spending and further pushes up demand and prices.

All 106 economists recently surveyed by Reuters expect the Federal Reserve to raise its benchmark overnight interest rate by 25 basis points to the range of 5.25%-5.50% this week, with the majority also predicting that this would be the final hike of the current tightening cycle.

ECB Monetary Policy Meeting

Thursday, July 27th. Decision at 12:15 PM GMT

After eight consecutive rate increases totaling 400 basis points since July 2022, investors and experts alike are engaged in a hot debate as to how many more rate hikes are required and how long rates must remain high to force inflation back to the 2% objective set by the ECB.

The Eurozone’s consumer price inflation rate was confirmed at 5.5% in June, the lowest level since January 2022, owing primarily to a drop in energy prices.

However, the core rate, which includes volatile goods such as food and energy, rose to 5.5% from 5.3% the month prior and exceeded forecasts.

This all but confirms for many the notion that ECB policymakers will continue to raise rates this month, and potentially again in September.

ECB President, Christine Lagarde, speaking recently at the ECB Forum on Central Banking in Sintra, Portugal, suggested that the concern lies in the fact that what was originally considered a transient inflation caused by energy shocks, has now permeated the wider economy and may persist.

According to minutes from the European Central Bank’s (ECB) June policy meeting, central bank officials generally agreed that the ECB would consider raising interest rates beyond July out of concern for prolonged high inflation, which raised doubts about achieving the inflation target any time soon. The ECB has stated that it will take a meeting-by-meeting approach in the face of a volatile economy and rising interest rates.

Economists recently polled by Reuters were unanimous that the ECB will raise interest rates by 25 basis points to 4.25% on July 27th, and most also anticipate a further increase at the September meeting.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk.

Comments are closed.