GBP/USD News and Analysis

Recommended by Richard Snow

Get Your Free GBP Forecast

US Q1 GDP Disappointment Does Little for Cable

US Q1 GDP missed estimates of 2% growth, coming in at a disappointing 1.1%. The print was the first estimate which typically has the greatest market-moving potential and notably, had very little effect after the release. In fact, cable has actually traded lower in the early afternoon during the London session despite a boost from Goldman Sachs who now anticipate a peak interest rate in the UK of 5%. Markets have priced in around 4.75% for the peak so the potential for a bullish repricing remains, particularly as rate expectations in the US took a hit after yesterday’s banking worries around another drastic decline in the share price of the fledgling First Republic Bank.

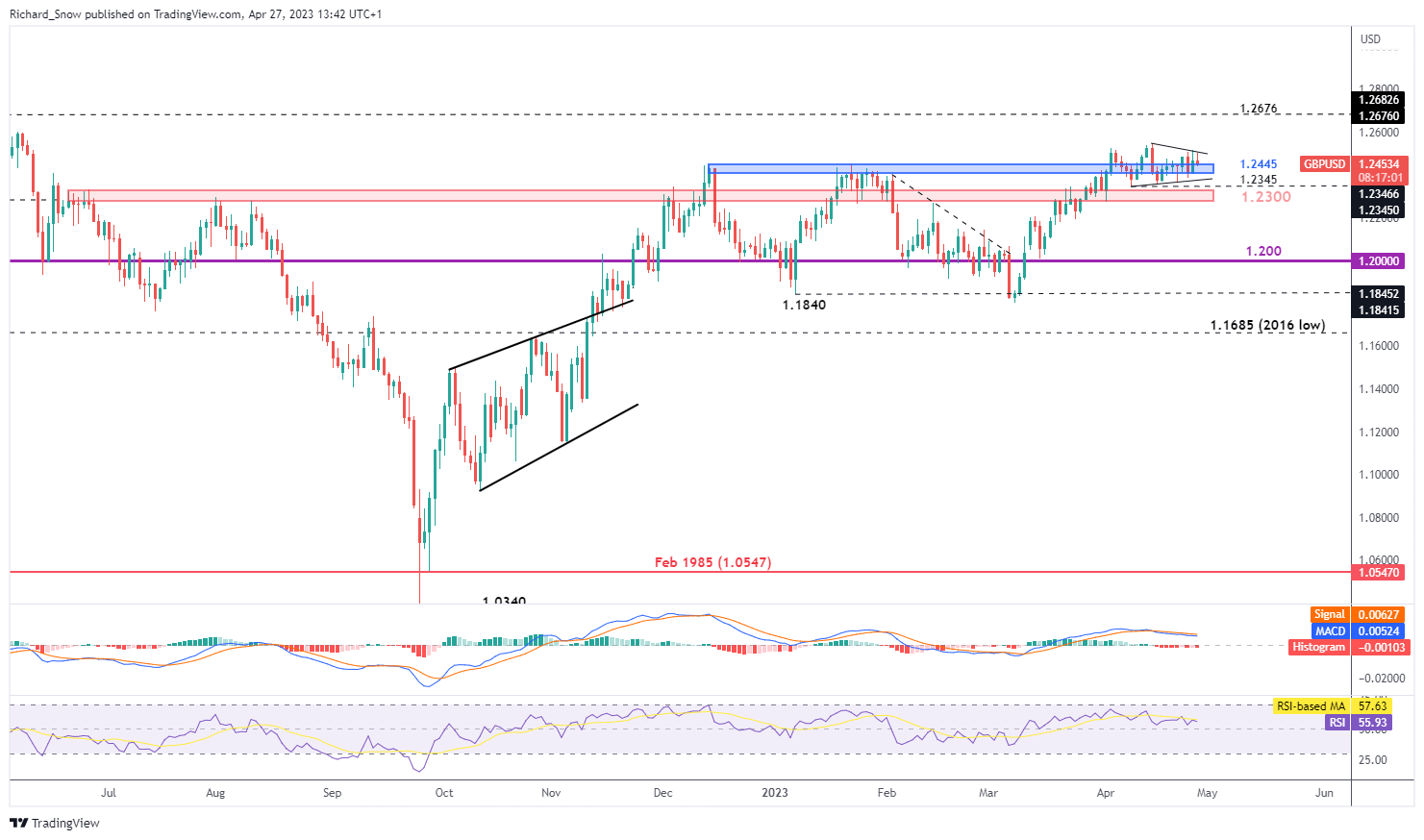

GBP/USD Technical Considerations and Levels of Interest

The technical outlook for cable suggest a lack of bullish momentum to set a new yearly high despite declining yields in the US and a rather forlorn US dollar. Yesterday and thus far today, extended upper wicks reveal a rejection of higher prices or at the very least, a reluctance to trade higher at current levels, in the absence of a catalyst. Keep in mind that the potential for a catalyst improves with the busy economic calendar in the next week.

Immediate support appears at the zone of support around 1.2445 followed by the underside of the wedge formation and 1.2345 and the zone around the psychological whole number of 1.2300. Resistance remains at the swing high of 1.2547.

GBP/USD Daily Chart

Source: TradingView, prepared by Richard Snow

Recommended by Richard Snow

Trading Forex News: The Strategy

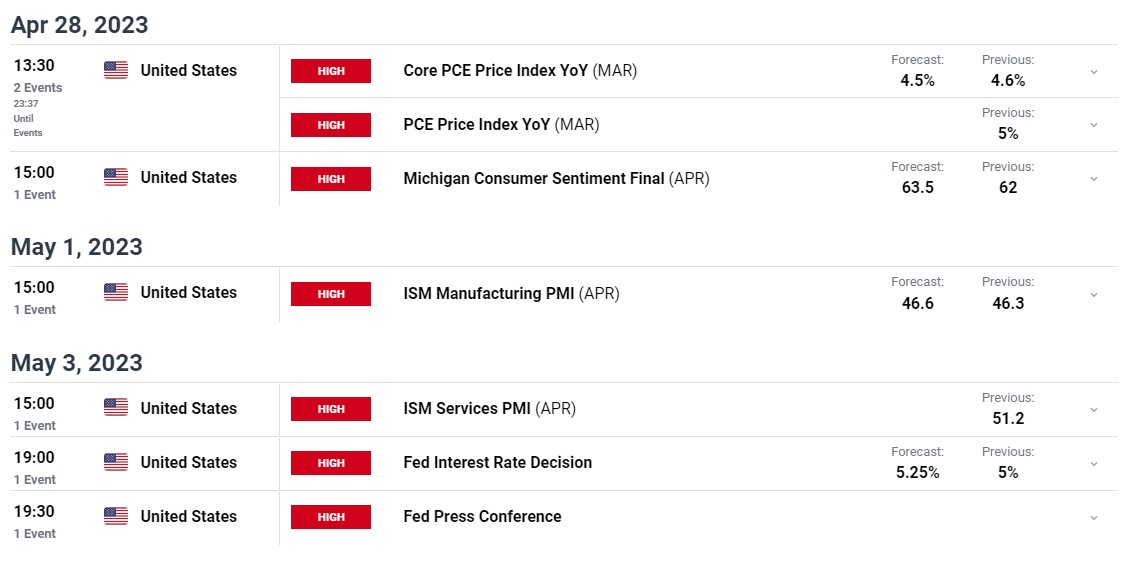

Major Risk Events for the Next Seven Days

After today’s US GDP data, tomorrow we’ll get the final piece of inflation data before the crucial FOMC meeting where markets have reduced the probability of a 25 basis point hike from Jerome Powell and the committee given the recent rise in uncertainty and slight lift in volatility. Hotter PCE data may revert those probabilities back in line with where they were a week earlier, however.

Additionally, both manufacturing and services PMI (ISM) are due next week where manufacturing lags the better-performing services sector – the major contributor to overall US GDP.

Customize and filter live economic data via our DailyFX economic calendar

— Written by Richard Snow for DailyFX.com

Contact and follow Richard on Twitter: @RichardSnowFX

Comments are closed.