ISM Non-Manufacturing (Services) PMI Misses Estimate

The second of the two measures gauging the health of the US economy compounded concerns that the relatively strong US economy is showing signs of concern. The ISM non-manufacturing PMI data came in at 51.2 vs expectations of 54.5 and a prior print of 55.1 in February.

Customize and filter live economic data via our DailyFX economic calendar

Signs of Concern Emerge for the US Economy

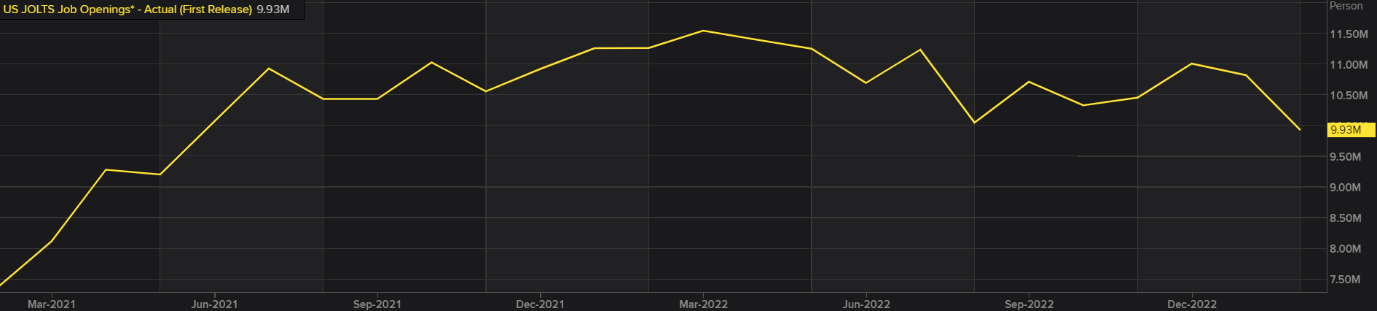

The disappointing US services data comes after the ISM manufacturing data plunged deeper into contractionary territory (46.3 from 47.7 in Feb), ADP employment data declined (145k vs 242 in Feb) and US job openings eased from 10.824 million to 9.931 million. While the data above likely reflects the uncertainty that ensued around the banking instability during the majority of March, the fact that the softer data is appearing across the board means this is certainly something that warrants further attention if recession concerns are to pick up from here.

Source Refinitiv

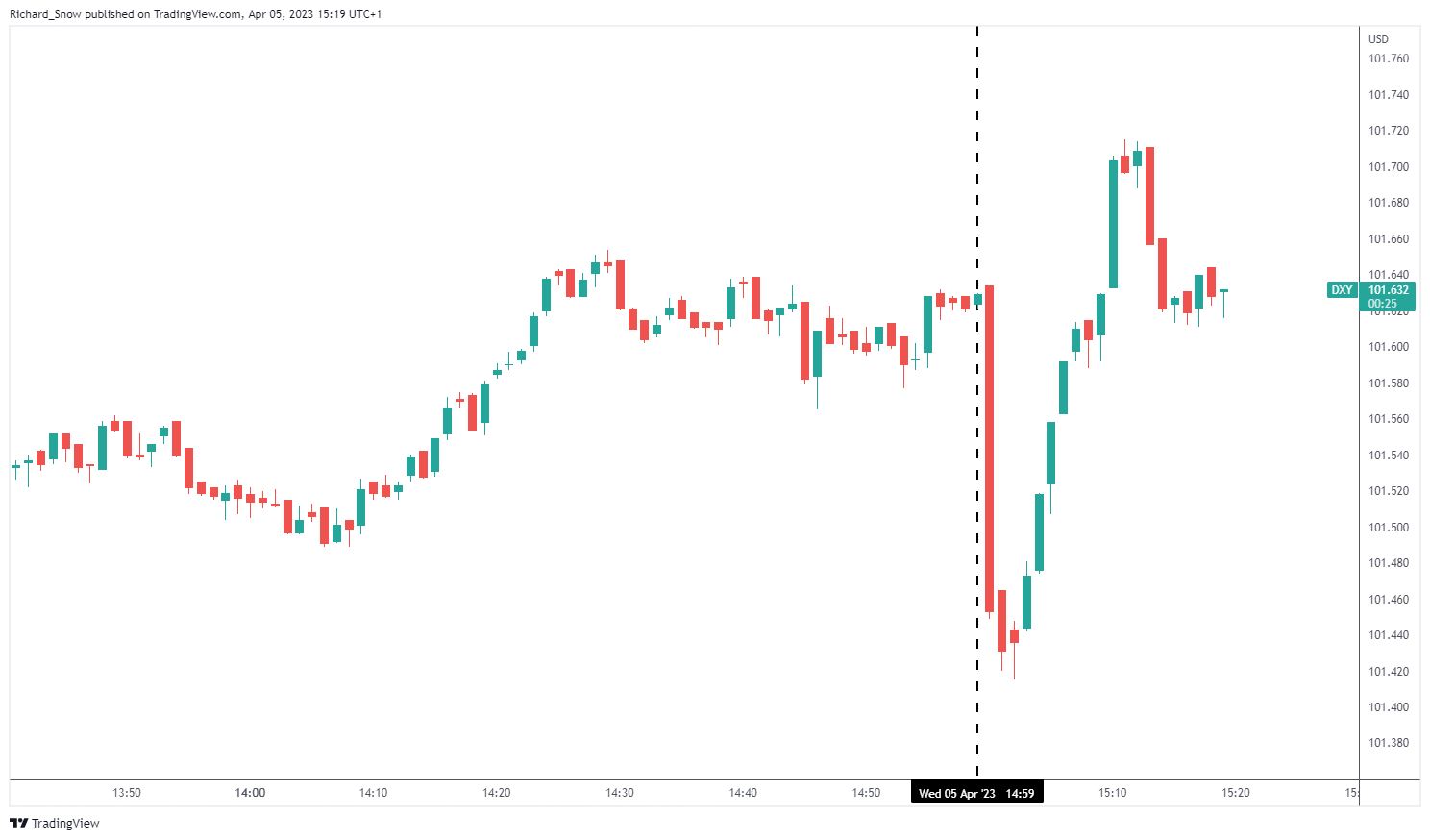

DXY (US Dollar Basket)

The dollar managed a recovery after initially declining in the moments after the data release. The US dollar is likely to be involved in a tug of war as growing market expectations of rate cuts in H2 keep the dollar suppressed, while on the other hand, the greenback still has safe-haven appeal (as data softens) and can rise on further hawkish rhetoric from Fed officials.

source: TradingView

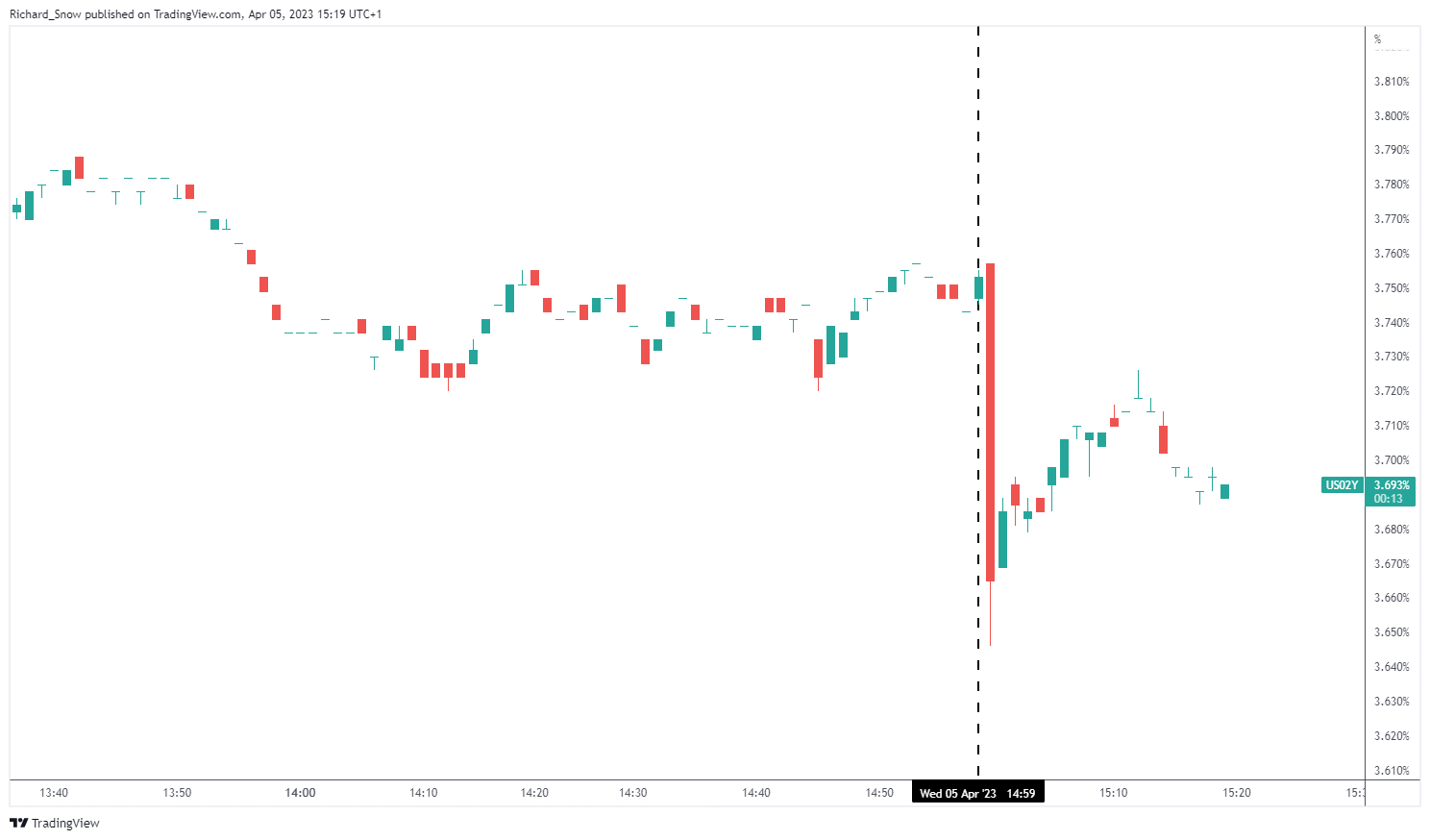

US 2-Year Yields

Rates on the shorter side of the yield curve, like the US dollar, saw an immediate drop but differs from the dollars response in that it has thus far been unable to rally back to levels witnessed prior to the data release.

source: TradingView

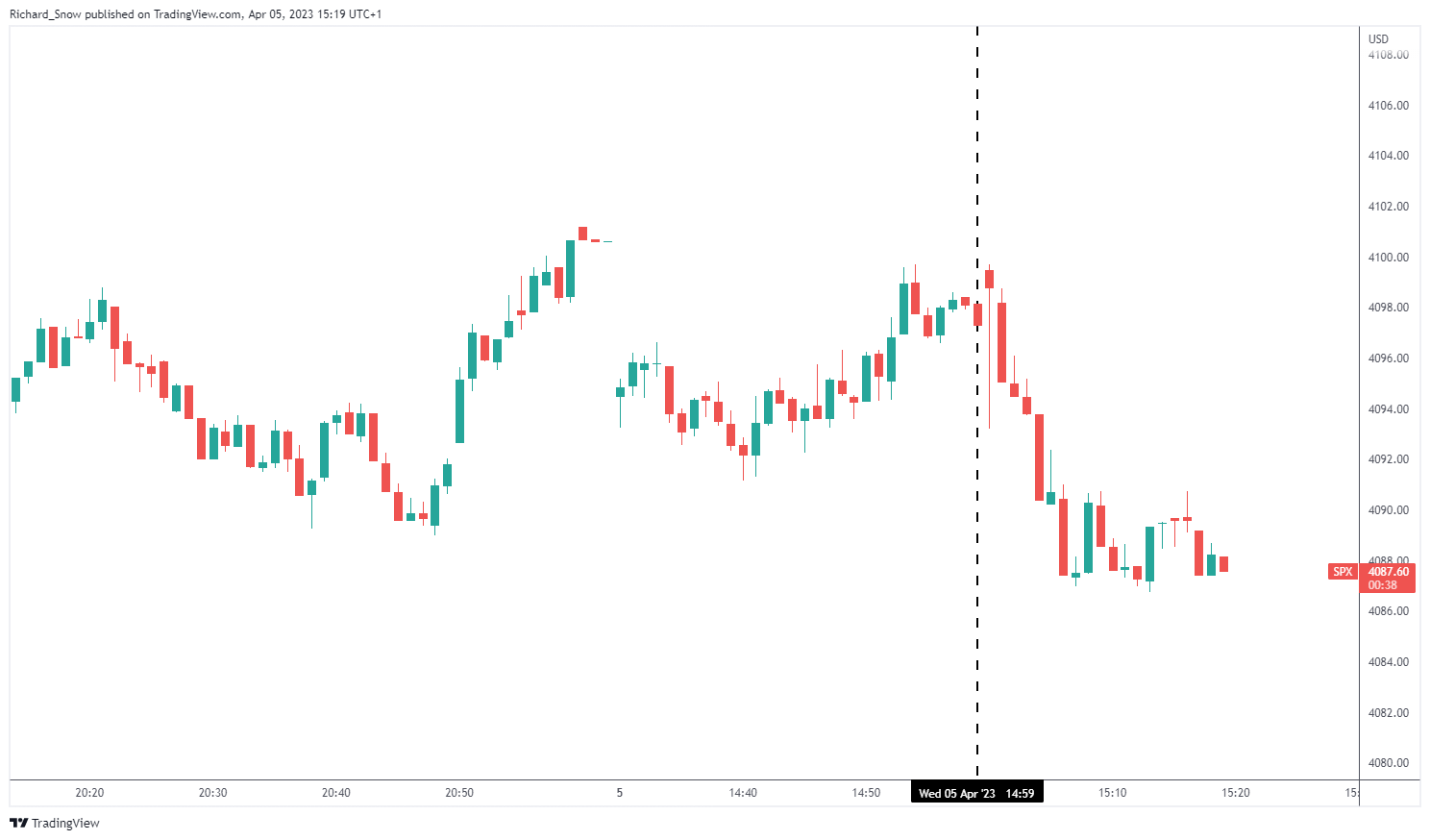

S&P 500

The S&P500 index eased after the release of the ISM services data, putting the index on course for a second day of declines. Before that, US equities were on quite the bullish run, rising as risk appetite returned to the market as recent support measures from the Fed eases concerns regarding US regional banks.

Next up on the calendar is US initial jobless claims – given the softer employment data this week – and US Non-farm Payrolls on Friday, which happens to occur over a public holiday meaning the potential for highly volatile moves remain a possibility considering lower expected liquidity.

— Written by Richard Snow for DailyFX.com

Contact and follow Richard on Twitter: @RichardSnowFX

Comments are closed.